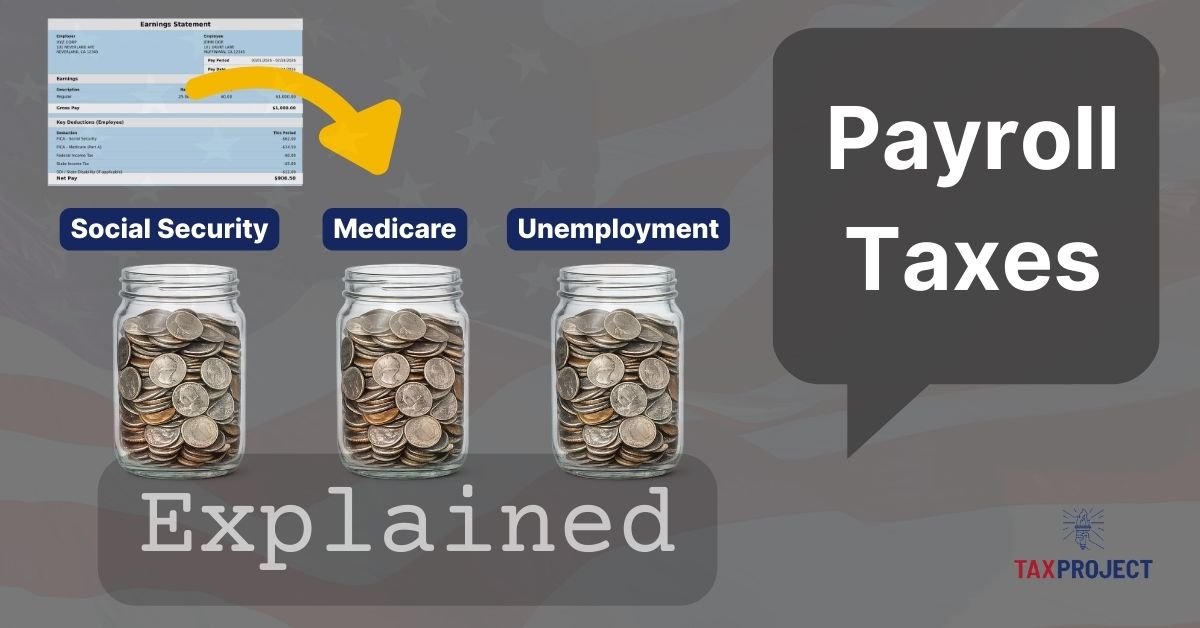

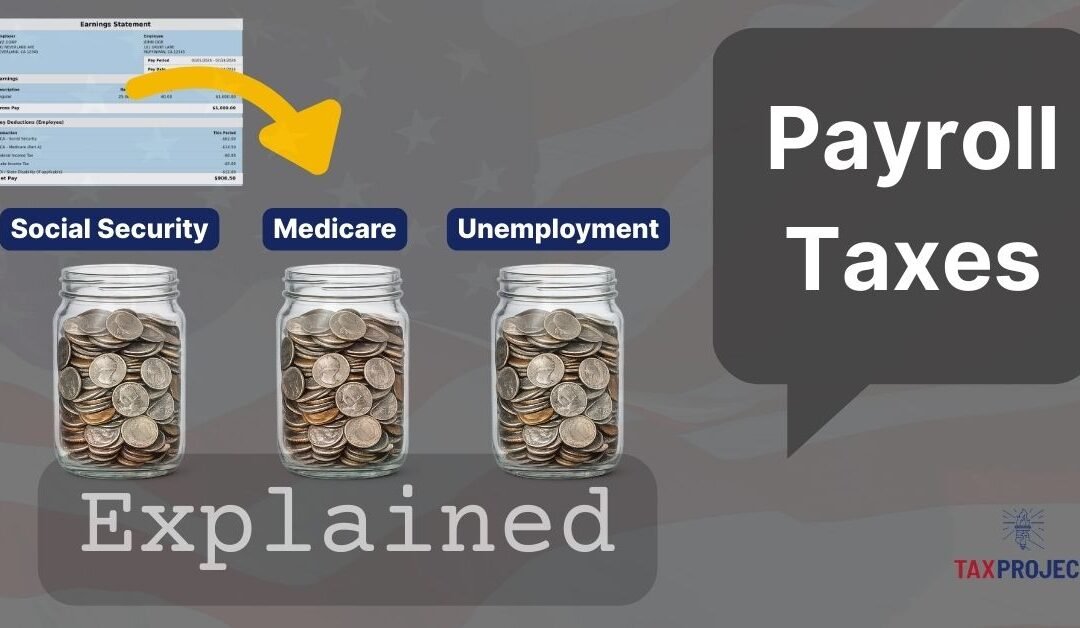

Payroll Taxes

Payroll taxes are taxes tied directly to wages and salaries. They are collected automatically through payroll withholding and employer payments, and they are the primary way the U.S. finances Social Security and part of Medicare, along with federal and state unemployment systems. In practice, payroll taxes are among the most “unavoidable” taxes for working households because they apply to paychecks from the first dollar of covered wages, regardless of whether you ultimately owe federal income tax.

This explainer covers (1) the purpose of payroll taxes, (2) payroll taxes vs other paystub withholdings, (3) the Federal, State, and Local components and how they’re calculated, (4) the employer share and why it matters, (5) a short history of how payroll taxes started, (6) where payroll taxes fit in the revenue picture, (7) and why payroll taxes are often regressive.

Payroll Tax History

The Modern U.S. Payroll Taxes grew out of the Great Depression era. They were part of the Franklin D. Roosevelt’s New Deal program introducing sweeping new social programs as part of America’s social safety net. The Social Security program was designed to support income in Old Age (Retirement), and a separate Federal Unemployment insurance framework. The Social Security Act was signed into law on August 14, 1935, and has continued to be updated ever since. In 1939 Survivor benefits were added, Disability benefits were part of the congress.gov/bill/84th-congress/house-bill/7225/titles" target="_blank" rel="noopener">Social Security Amendments of 1956 after a disability freeze was created in 1954. Payroll taxes began to be collected in 1937, and monthly benefits began in 1940. [7]

Why Payroll Taxes were designed this way: policymakers wanted a long term structural financing mechanism tied to work, with contributions from both Workers and Employers. That approach created a dedicated funding stream and helped define the program as earned social insurance.

Unemployment insurance also developed as a Federal-State system financed largely through Employer payroll taxes, with Federal FUTA operating as a Federal layer and States running their own benefit systems and tax structures. [5] [6]

Purpose of Payroll Taxes

Payroll taxes exist to fund specific “social insurance” programs tied to work. The idea is that when you earn wages, you and your employer contribute to programs that provide benefits during retirement (and for survivors and disability) and provide income support during periods of unemployment. That design matters because it explains why payroll taxes are structured as a percentage of wages, why they show up separately from income taxes, and why some parts have cap limits or thresholds.

Social Security, for example, is financed primarily through payroll contributions. It was designed as contributory insurance tied to earnings and work history, rather than being funded solely through general income taxes. That “contributions for benefits” framing is baked into how the taxes are calculated and how the programs are discussed in policy debates. [1]

Payroll Taxes vs “Everything Withheld”

A paystub can look like a pile of taxes and deductions, but it helps to separate them into three categories:

- Payroll taxes (the focus of this article): wage-based taxes that fund Social Security, Medicare, and unemployment programs. [2]

- Income tax withholding: Federal income tax (and sometimes State/Local income tax) withheld from paychecks as a prepayment of your income tax liability. These are not “payroll” taxes even though they’re withheld by payroll.

- Deductions: health insurance premiums, retirement contributions, HSA/FSA contributions, and other benefit deductions. These aren’t taxes, though they can affect “taxable wages” for certain taxes depending on the type of benefit.

The Internal Revenue Service (IRS) often uses the broader term employment taxes to describe the full set of tax responsibilities connected to wages (withholding, depositing, and reporting). IRS Publication 15 is a primary reference employers use for these rules. [3]

“Covered wages” means wages that are subject to a specific payroll tax (for example, wages subject to FICA, FUTA, or state unemployment tax rules).

Payroll Tax Components

When you look at your pay stub you will likely see a whole bunch of acronyms and line items. These come from both the Federal Government and State/Local Governments. They use a lot of acronyms and some of them are shorthand for more than one component. Here are the components you will see in some form or another on your stubs.

Federal Payroll Taxes (core components)

FICA (Federal Insurance Contributions Act):

The Federal Payroll Taxes for Social Security and Medicare that are withheld from wages (and matched by employers). Items 1–3 below are FICA taxes: Social Security and Medicare, including the Additional Medicare Tax that applies to higher earnings. [3]

1) Social Security Tax – Old-Age, Survivors, and Disability Insurance (OASDI)

- Rate: 6.2% withheld from employees and 6.2% paid by employers. [1]

- Wage base (cap): Social Security tax applies only up to a maximum amount of wages each year. For earnings in 2026, the Social Security wage base is $184,500. [1]

- What you see: When your year-to-date wages cross the wage base, Social Security withholding stops for the rest of that calendar year. [2]

Simple formula (employee side):

Social Security tax = 6.2% × wages up to wage base [1]

2) Medicare Tax (Part A / Hospital Insurance)

- Rate: 1.45% withheld from employees and 1.45% paid by employers. [2]

- No wage cap: Medicare tax applies to all covered wages, unlike Social Security. [2]

Simple formula (employee side):

Medicare tax = 1.45% × wages [2]

3) Additional Medicare Tax (0.9% surtax)

- Rate: An additional 0.9% on Medicare wages above certain thresholds which vary by filing status (see Table 1). [4]

- Employer withholding rule: Employers must begin withholding the additional 0.9% once an employee’s wages paid by that employer exceed $200,000 in a calendar year, regardless of filing status. [4]

Simple formula (conceptual):

Additional Medicare Tax = 0.9% × wages above the applicable threshold [4]

| Filing Status | Threshold |

|---|---|

| Single | $200K |

| Married filing jointly | $250K |

| Married filing separately | $125K |

4) Federal Unemployment Tax (FUTA)

- Who pays: Employer-paid (not withheld from employees). [5]

- Basic structure: The standard FUTA tax rate is 6.0% on the first $7,000 of wages per employee per year. [5]

- Credits: Employers typically receive credits for state unemployment taxes paid, often reducing the effective FUTA rate substantially (with exceptions in “credit reduction” situations). [5]

State Payroll Taxes (core components)

5) State Disability Insurance (SDI)

- Who pays: Varies by state; commonly employee-paid via paycheck withholding (and in some states employer-paid or split). [6]

- Basic structure: A state-run insurance program funded through payroll contributions in some states that provides partial wage replacement when a worker can’t work due to a non-work-related illness or injury (and, in some states, certain pregnancy-related conditions). [6]

- What you see: Often appears as “SDI” (or similar) on a paystub in states that run a disability insurance program. [6]

Simple formula (conceptual):

SDI contribution = SDI rate × taxable wages (subject to state rules and any wage base). [6]

6) Paid Family Leave (PFL)

- Who pays: Varies by state; commonly employee-paid via paycheck withholding (and in some states employer-paid or split). [6]

- Basic structure: A state-run program funded through payroll contributions in some states that provides partial wage replacement when a worker takes qualifying family or caregiving leave (for example, bonding with a new child or caring for a seriously ill family member). [6]

- What you see: Often appears as “PFL” (or a related label) on a paystub in states that offer paid family leave funded through payroll contributions. [6]

Simple formula (conceptual):

PFL contribution = PFL rate × taxable wages (subject to state rules and any wage base). [6]

7) State Unemployment Insurance / Unemployment Insurance (SUI/UI)

All states run unemployment insurance systems, but state payroll taxes vary widely. The biggest state Payroll tax category is State Unemployment Insurance (SUI/UI). In most cases:

- Who pays: It is primarily employer-paid

- Rate: The rate varies by employer

- Wage base (cap): The taxable wage base varies by state, and Employers may also face additional state payroll contributions depending on state programs. [6]

Local Payroll Taxes

8) Local Payroll Taxes

Local Payroll taxes aren’t universal, however, they do exist and some cities and counties impose payroll-based taxes (often framed as employer payroll expense taxes). Local payroll taxes exist in a few jurisdictions and are highly location specific.

How the Math Works

For most W-2 workers (not self-employed), Payroll Taxes are calculated based on covered wages, and the amounts are split into:

- EMPLOYEE Withholding: Social Security, Medicare, and possibly Additional Medicare Tax

- EMPLOYER Paid Payroll Taxes: Employer match for Social Security and Medicare, plus FUTA and State/Local Employer Payroll taxes. [2] [3]

If you remember one thing: your paystub shows the employee side, but employers typically pay meaningful payroll taxes on your behalf on top of your gross wage that you never see on your pay stub. [3]

Payroll Tax Calculator

Try our Payroll Tax Calculator to estimate your Payroll Taxes*

Employer Paid Payroll Taxes

Payroll taxes are often discussed like they’re only the amounts withheld from your paycheck. That’s incomplete. Whether you know it or not, Employers are required to pay significant portions of Payroll taxes on your behalf.

Employers typically pay:

- Employer Social Security: 6.2% up to the wage base. [1]

- Employer Medicare: 1.45% on all covered wages. [2]

- Federal Unemployment Tax Act (FUTA): employer-only federal unemployment tax, subject to credits. [5]

- State Unemployment Insurance/Unemployment Insurance (SUI/UI): and other state/local payroll programs: usually employer-paid and highly variable. [6]

Why this matters for workers: the employer share affects the total cost of employing someone. Over time, employers tend to think in “all-in” labor cost terms (wages + payroll taxes + benefits). You don’t need an economics lecture to see the implication: if the employer’s cost of employing a worker rises, that can influence wage offers, hiring decisions, depress future wage growth, or how compensation is allocated between cash wages and benefits.

*NOTE – Self-employed generally pay self-employment tax (Self-Employment Contributions Act – SECA) that roughly covers both employee + employer halves of Social Security and Medicare.

Where do Payroll Taxes fit?

Payroll taxes are a major source of Revenue in the Federal budget. A Congressional Research Service overview reports that in FY2023, payroll taxes generated $1.6 trillion, or 36% of total Federal revenue, making Payroll taxes the second-largest revenue source after individual income taxes. [8]

Because payroll taxes are such a large source of federal revenue, they’re central to how Social Security and Medicare are financed. Even small changes to payroll tax rates or the wage base can meaningfully change how much money those programs bring in over time.

Payroll Taxes are often Regressive

A tax is commonly called regressive when lower-income households pay a higher share of their income in that tax than higher-income households. It doesn’t mean they pay more or a higher rate, but as a percentage of their income it represents a higher share. Payroll taxes often fit that description, mainly because of how Social Security is structured and how different households earn income.

Two key drivers:

- The Social Security wage cap. Social Security tax applies only up to an annual wage base. Above the wage base cap limit, the 6.2% employee tax stops (and the employer match stops too), which lowers the effective Social Security tax rate as wages rise beyond the cap. [1]

- Payroll taxes focus on wages. Payroll taxes generally apply to wage and salary income, not to most investment income (such as capital gains), which tends to be a larger share of income for higher-income households. [9]

There’s an important nuance: Medicare taxes are less regressive than Social Security taxes because Medicare has no wage cap and includes an additional surtax above certain thresholds. [2] [4] That doesn’t eliminate regressivity overall, but it changes the shape: the “cap effect” is primarily a Social Security issue.

Payroll Taxes FAQ

- Why did my Social Security withholding stop late in the year?

Because Social Security tax applies only up to the annual wage base. In 2026, the wage base is $184,500. [1] - Why does Medicare keep being withheld even after Social Security stops?

Because Medicare has no wage cap; it applies to all covered wages. [2] - Why did my employer start withholding an extra 0.9% Medicare tax?

Because employers must withhold Additional Medicare Tax once wages paid by that employer exceed $200,000 in the calendar year. [4] - If I have two jobs, can I pay too much Social Security tax?

Yes. Each employer withholds up to the wage base as if it’s your only job. Over-withheld Social Security across multiple employers is handled as a credit/refund on Form 1040. [2] - Are bonuses subject to payroll taxes?

In general, most cash compensation treated as wages is subject to Social Security and Medicare under IRS wage rules, with specifics governed by employer payroll guidance. [3] - Do independent contractors pay payroll taxes?

Contractors generally don’t have payroll withholding like W-2 employees, but they may owe self-employment taxes and make estimated tax payments depending on their situation. [3]

Summary

Payroll taxes were introduced during the Great Depression part of the New Deal and fund core social insurance and unemployment programs and make up a major component of the American Social Safety net. Both you and your employer pay into these programs. Your employer treats these payments as part of your total compensation and benefits. They include what you see withheld from your paycheck and a significant employer paid amount that usually isn’t visible. Payroll taxes are the second largest source of Federal revenue after Income taxes.

References

- Social Security Administration. 2026. “Contribution and Benefit Base.” SSA Office of the Chief Actuary. Retrieved February 14, 2026 (https://www.ssa.gov/oact/cola/cbb.html). (Social Security)

- Internal Revenue Service. 2026. “Social Security and Medicare Withholding Rates (Topic No. 751).” Retrieved February 14, 2026 (https://www.irs.gov/taxtopics/tc751). (IRS)

- Internal Revenue Service. 2026. Publication 15 (Circular E), Employer’s Tax Guide. Washington, DC: Internal Revenue Service. Retrieved February 14, 2026 (https://www.irs.gov/publications/p15). (IRS)

- Internal Revenue Service. 2025. “Additional Medicare Tax (Topic No. 560).” Retrieved February 14, 2026 (https://www.irs.gov/taxtopics/tc560). (IRS)

- Internal Revenue Service. 2025. “FUTA Credit Reduction.” Retrieved February 14, 2026 (https://www.irs.gov/businesses/small-businesses-self-employed/futa-credit-reduction). (IRS)

- U.S. Department of Labor, Employment and Training Administration. n.d. “Unemployment Insurance Tax Topic.” Office of Unemployment Insurance. Retrieved February 14, 2026 (https://oui.doleta.gov/unemploy/uitaxtopic.asp).

- Social Security Administration. n.d. “Social Security History FAQs.” Retrieved February 14, 2026 (https://www.ssa.gov/history/hfaq.html).

- Congressional Research Service. 2024. Overview of the Federal Tax System in 2024. R48313. Washington, DC: Congressional Research Service. Retrieved February 14, 2026 (https://www.congress.gov/crs-product/R48313).

- Tax Policy Center. n.d. “Are Federal Taxes Progressive?” Retrieved February 14, 2026 (https://taxpolicycenter.org/briefing-book/are-federal-taxes-progressive).

*Estimate Only – for illustration purposes only, should not be used as an official use. Contact your Accountant or Tax professional for guidance. The Tax Project Institute is not a Government entity, and not associated with the IRS, Social Security Administration, or Medicare.