In a healthy Economic environment the Central Bank of a country, the Federal Reserve (Fed) in the United States, manages the Monetary Policy that manages the money supply, and sets interest rates to keep inflation under control and the job market healthy. The Federal Reserve is said to have a dual mandate to maintain stable pricing (manage Inflation), and maximum employment (stable Jobs). While elected officials in the Executive Branch and Congress manage the Fiscal Policy that sets taxes and the budget that determines spending. These functions are setup as independent processes with different goals.

Fiscal Dominance is a term used when a Country’s Debt and Deficits get so large that Fiscal Policy begins to, either explicitly or implicitly, steer Monetary Policy. This can be a very troublesome situation to be in because it puts two competing responsibilities into conflict at times, and in general should be avoided where possible because of the risks involved. In high debt environments, interest payments on the debt can become very large and begin to crowd out other Government spending. As the interest rates raise, the debt payments grow and compound the challenges. This can put pressure on the Fed to go against their mandate to lower interest rates and thereby reduce the cost of the debt service payments. However, by lowering rates the Fed may lose control on Inflation which may rise higher than their target rate.

Former Treasury Secretary and Federal Reserve Chair Janet Yellen defines it as when deficits and debt put so much pressure on the government’s financing needs that Monetary Policy becomes “subordinate” to those needs, meaning the central bank is pushed to keep rates “lower than warranted” or buy government debt “to ease the government’s financing burden.” [1]

The challenge is that inflation becomes the easiest way out because it can immediately reduce the cost of debt service and quietly shrink the real value of what the Government owes. This is a lot easier for elected officials than raising taxes, cutting spending, or changing entitlement programs due to the unpopularity with constituents. However, through inflation it also shrinks the buying power of everyone’s dollars.

“If congress is unable or unwilling to address primary deficits the problems will compound and the temptation to rely on inflation or financial repression to reduce the debt burden will surely grow.”

Janet Yellen , “The Future of the Fed” January 4-5, 2026 [1]

Why does it Matter?

Since the COVID pandemic, after a long period of stable pricing, the US experienced higher than normal inflation, and most Americans now understand inflation, and what is being called the “Affordability Crisis” as something much more tangible and real. Inflation is no longer an abstract statistic. It is the slow (or sometimes fast) loss of what your money can buy. The Bureau of Labor Statistics tracks prices with the Consumer Price Index and explains inflation as when prices rise, the purchasing power of the dollar declines. [4]

The damage caused by inflation shows up everywhere: groceries, gas, rent, insurance, childcare, car repairs. If pay does not keep up with inflation then living standards slip. If you hold cash or earn a low interest rate on savings, inflation reduces the value of your money punishing savers, those on fixed income, and the most vulnerable.

You can also see inflation worry show up in markets. When people get uneasy about the future buying power of dollars, they often look for hedges. Gold is the classic example. Recently Gold has been hitting record highs above $5,000/oz in late January 2026, driven by safe-haven demand and uncertainty, along with expectations about interest rates and heavy Federal Reserve buying. [3]

None of this is to say Fiscal dominance is happening now, but as Janet Yellen recently said “the preconditions…are clearly strengthening.” (See Janet Yellen Statements here)

“the preconditions for fiscal dominance are clearly strengthening”

Janet Yellen, “The Future of the Fed” January 4-5, 2026 [1]

“I doubt Americans will wind up on the Fiscal Dominance course, but I definitely think the dangers are real and should be monitored.”

Janet Yellen , “The Future of the Fed” January 4-5, 2026 [1]

The risks are not about political parties, or politicians, but basic math. Here are some of the challenges:

When Debt is High, Interest Increases Hurt!

When the government owes a lot, even modest levels of debt can become expensive with high interest rates. That expense to pay the rising interest cost on debt competes with everything else the government wants to do. For every 1% increase in interest rates debt service costs increase nearly $400 billion annually. [6] (See Table 1 below)

The Congressional Budget Office’s (CBO) February 2026 outlook (summarized by the Committee for a Responsible Federal Budget) shows debt held by the public around 100% of GDP (i.e. the entire US Economy) and projected to rise to about 120% by 2036. It also shows Net Interest costs (the amount we pay on debt) more than doubling from ~$970 billion in 2025 to about ~$2.1 trillion by 2036, rising from about 3.2% of GDP to about 4.6% of GDP. [2]

High Interest Costs Squeeze Budgets

Unlike many budget expenses, interest is the part you pay because of past spending. It does not build roads, improve schools, or provide services directly. As it grows, it can crowd out other priorities or force harder choices later.

The current Net Interest is larger than the expense of the US Military, so doubling that cost would be a very large expense putting pressure on other spending. Whether someone sees those numbers as “manageable” or “dangerous,” they are big enough to create strong political pressure around interest rates.

This is where Fiscal Dominance risk starts to become realistic: if interest costs feel like they are exploding, it becomes politically tempting to push for lower rates regardless of inflation conditions.

The Catch-22: Debt Service vs Inflation

For younger folks a Catch-22 is a situation with no good options. You’re dammed if you do, and dammed if you don’t.

Here is the doom loop in simple steps:

Inflation is too high, or the risk of inflation is rising.

The Fed raises rates to slow inflation and protect the value of the dollar.

Higher rates raise the government’s interest bill over time.

The higher interest rate increases debt service cost that squeezes the budget.

Pressure rises to lower rates to “stop the bleeding” and lower interest costs.

If rates are cut too soon, inflation can come back, and the cycle repeats.

Yellen’s warning is that when the central bank is constrained from raising rates because it would increase debt service or cause fiscal stress, inflation expectations can become “unanchored,” and people may start to think inflation is the “path of least resistance” for managing high debts. [1]

That phrase is worth translating: once a society starts to believe “they will inflate rather than make hard choices,” the value of money becomes a political variable. That is when inflation becomes harder to control.

Interest rate

Estimated Net Interest

Delta vs Current

1%

$0.39T

-$0.93T

2%

$0.77T

-$0.54T

3%

$1.16T

-$0.15T

Current (3.4%)

$1.31T

$0.00T

4%

$1.55T

+$0.23T

5%

$1.93T

+$0.62T

10%

$3.86T

+$2.55T

15%

$5.80T

+$4.48T

20%

$7.73T

+$6.42T

Table 1 Estimated Net Interest

Can Both Sides be Right and Wrong?

It can be hard in our polarized environment not to think about this as either one side is Right or Wrong, however that misses the point. Both Fiscal and Monetary policy play important roles in the Economy and impact all Americans. Normally these can operate independently and support each other, a sort of Yin and Yang that balance each other out. The challenge when Debt and Spending get so large that they put Monetary and Fiscal responsibilities into conflict.

Fiscal Policy: Executive Branch and Congress

What they care about: Spending (Debt service) and Growth

Why they can be Right:

Lower Interest costs can reduce Net Interest expenses that crowd out other spending and make the budget fragile.

Lower rates can support growth that can expand the tax base and reduce immediate fiscal strain.

Why they can be Wrong:

By leaning on the Fed to lower Interest rates they may increase inflation and reduce the value of the dollar.

Monetary Policy: The Federal Reserve

What the Fed cares about: Stable Pricing (Inflation) and Maximum Employment (Jobs)

Why the Fed is Right:

Protecting purchasing power is not a luxury. When inflation is unstable, everyone lives with more uncertainty, borrowing costs and the Affordability crisis increase, and the value of the dollar diminishes.

Yellen makes the key point that “stabilizing prices becomes significantly more costly” once inflation expectations take hold. [1]

Why the Fed can be Wrong:

Tightening policy in a high-debt environment can create political backlash and institutional stress. Even if the Fed’s policy is “correct” on inflation, it can still trigger a fight over Fed independence that changes the rules of the game.

Short term priorities due to massively rising Debt Service costs may pose greater danger than long term rising inflation.

This is the core Catch-22: the fiscal side is not crazy to care about interest costs, and the Fed is not crazy to prioritize inflation. Inflation can be a lot like a heart attack, it can go quietly unnoticed but suddenly impact you. By letting inflation slowly (or quickly) devalue the dollar, everything gets more expensive and your savings are worth less.

What does Fiscal Dominance look like?

Fiscal dominance usually does not arrive with a press release. It shows up as a drift in behavior and expectations, such as:

Repeated pressure to cut rates mainly to reduce the government’s borrowing costs.

A growing expectation that the central bank will not do what it takes to control inflation if it would make the budget painful.

Challenges to the Federal Reserve autonomy

Investors demand compensation to cover the additional Risk Premia because they worry the government will rely on inflation to manage the debt, devaluing the dollar.

Yellen’s Listed Preconditions

Steep upward debt trajectory: CBO projects debt rising from ~100% of GDP in 2026 to over 150% in three decades—current levels already test sustainability.

Persistent large deficits: ~6% of GDP overall (~3% primary), unprecedented outside wars/recessions, with no credible medium-term fiscal adjustment plan from either party.

Debt service pressure on monetary policy: When debt hits ~120%+ GDP, rate hikes to fight inflation risk exploding interest costs, forcing Fed to prioritize debt financing over its dual mandate.

Yellen flags the same idea: fiscal dominance can raise borrowing costs if investors become concerned the government will rely on “inflation or financial repression” to manage debt. [1]

“Kick the can down the Road”

Many Western Democracies are trapped in a similar situation: High Debt, Growing Entitlements, Limited will to Raise Taxes or Cut Spending. It is politically far easier to postpone painful choices. Nobody wants higher taxes. Nobody wants spending cuts. Nobody wants entitlement changes. That political reality is not a moral failing; it is a constraint.

However, the longer we stay on our current fiscal path and our debt continues to grow, the more painful the eventual adjustment will be. This is not a problem that goes away on its own. Yellen states the hard version of this idea: if markets do not expect future budget surpluses to cover the debt, “the adjustment eventually comes via inflation or default.” [1]

For the U.S., “default” is not the scenario most people think about, although all three rating agencies have downgraded the US [5]. The more realistic concern is a mix of:

Higher Inflation – everything will cost more, and your money will be worth less

Higher Borrowing Costs – credit will cost more

Forced Fiscal Changes – some combination of tax increases and/or spending cuts

This is why Fiscal Dominance is not just a “Fed independence” topic. It is about whether the country chooses a gradual planned path or dramatic unplanned (but predictable) one. (See our Article: Ways out of Debt)

Summary

Fiscal Dominance is not a slogan and it is not “here” yet. It is a risk that grows when debt is high, and interest costs are large, and political incentives push for easier money even when inflation is not truly under control. The stakes are high, we can begin to manage it now, or we risk higher inflation and the devaluation of the dollar and the cost of everything increasing.

Citation

[1] Janet Yellen, “Remarks on the future of the Fed: Central bank independence and fiscal dominance” (Brookings, Jan 2026). (Brookings) [2] CBO February 2026 outlook summary (Committee for a Responsible Federal Budget, Feb 11, 2026). (CRFB) [3] “Gold jumps over 3% to record peak…” (Reuters, Jan 27, 2026). (Reuters) [4] BLS CPI FAQ and purchasing power notes (BLS). (Bureau of Labor Statistics) [5] CNN. May 2025. “The United States just lost its last perfect credit rating.” (CNN) [6] Based on US Treasury Debt to Penny 2/12/26, average rate on interest-bearing debt 12/4/25 Peterson Foundation

See how well you understand the Finances of America. Every American should understand the basic components of how our Government manages the finances of the Country. Only through knowledge are we able to understand the financial state of the country, and thus the health of the country and from this knowledge the ability to make informed decisions.

“Knowledge will forever govern ignorance; and a people who mean to be their own governors must arm themselves with the power which knowledge gives.”

James Madison

Test Government Finance Knowledge

About how much Revenue does the U.S. Federal government collect in a typical recent year?

Order of magnitude: Federal revenues are in the mid single-digit trillions, not billions. For example, in Fiscal year 2024 the federal government collected about $4.9 trillion in revenue. That was just under 20% of U.S. GDP for that year. Learn more: Federal Revenue overview.

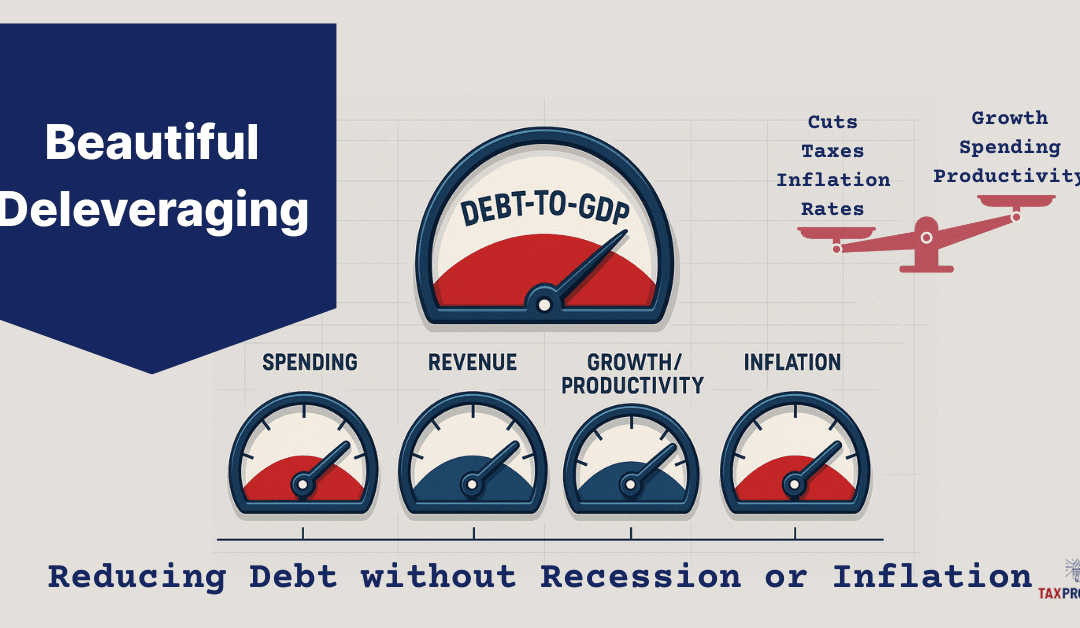

How the U.S. Could Reduce Debt Without Breaking the Economy

The U.S. National Debt just passed $38 trillion according to the US Treasury’s Debt to the Penny. [1][2] Not all debt is bad, but if it gets too large then debt can matter a lot, even those denominated in a fiat currency, because interest costs compound and grow they can crowd out other national priorities. Growing up your parents may have told you that it’s a lot easier to get into something, then to get out. That is especially true for debt, easy to get in, and painful to get out. Now that we have reached the point where interest payments are over $1 trillion annually, the US has crossed into that uncomfortable territory. The real challenge is to bring debt growth under control without causing a recession or a bout of high inflation. Ray Dalio, a billionaire hedge fund manager who has written books on Why Nations Succeed and Fail, and How Countries go Broke, popularized the idea of a “Beautiful Deleveraging” – a balanced, multi-year process that reduces the painful process of deleveraging when lowering debt burdens through a mix of growth, moderate inflation, controlled austerity, and targeted debt adjustments, rather than a painful deleveraging that could lead to recession, extreme reductions in services, tax increases, and austerity measures. [3][4]

This piece frames what a Beautiful Deleveraging could look like for the United States, why it’s hard, the challenges faced, and how policy could balance the Deflationary forces of tightening with the Inflationary tools sometimes used to ease the adjustment—aiming for a soft landing that improves the country’s long-run fiscal and economic health, while minimizing the pain along the way.

Current Status

National Debt: The National Debt stands at just over $38 trillion (gross) with over $30 trillion of which is Debt held by the public. [2]

Deficits: Structural Annual deficits running over $1trillion at around ~6% of GDP. [5][6]

Interest Costs: Net Interest over $1 trillion annually. The Congressional Budget Office (CBO) Long-Term Budget Outlook (March 2025), Net Interest reaches 5.4% of GDP by 2055, up from ~3.2% of GDP around 2025. [7][8] Independent analysis by the Committee for a Responsible Federal Budget (CRFB) highlights a related pressure point: by the 2050s, net interest would consume roughly 28% of federal revenues, absent policy changes. [9]

According to CBO’s latest long-term outlook, by 2055 total Federal outlays (spending) are projected at about 26.6% of GDP, with Net Interest (interest paid on National Debt) near 5.4% of GDP. That means that roughly one-fifth (~20%) of Federal spending will be used to pay interest on the debt. At that scale, interest costs rival or exceed most standalone programs and risk crowding out other priorities if unaddressed. [7][8][9]

What “Beautiful Deleveraging” Means

In Economic terms, Beauty is about reducing debt while avoiding (or at least minimizing) the painful parts of deleveraging and therefore managing that successfully can be Beautiful. Dalio’s Deleveraging framework was originally developed to explain past debt cycles and emphasizes a balanced mix of tools so that the economy can reduce debt without crashing demand and involves these components:

Spending Restraint (public and private demand constraint),

Income growth (real GDP growth),

Debt Restructuring or Terming out (Monetary intervention when necessary), and

A measured amount of Money/Credit creation (Moderating and managing inflation).

These components, when executed with great skill, political courage, and balance, can help the economy grow enough to ease debt ratios while avoiding a deflationary spiral. [3][4]

For a sovereign like the U.S., that balance translates into a policy with credible fiscal consolidation, productivity-oriented growth policies, and a monetary policy that avoids both runaway inflation and hard-landing deflation. Because the U.S. issues debt in its own currency with deep capital markets, it has more room to maneuver than most, but it is not immune to arithmetic: if interest rates (R) run above growth (G) (See our Article on R > G), debt ratios tend to rise unless deficits are reduced. CBO’s long-term projections foresee precisely this pressure in their future outlook. [9]

Pain Points: Why Deleveraging Is Hard

There is a reason it’s hard, in general large broad spending cuts, and more and higher taxes are not popular. While the components and levers are well known, it takes a healthy amount of political courage to propose policies that maybe unpopular, a great deal of skill and coordination to execute these policies, and likely a good amount of luck and good timing for a sustained period likely across several administrations. A deleveraging can proceed along two of these painful paths, spending cuts and tax increases, and each has tangible real-world consequences:

Spending cuts: Less public consumption and investment, fewer or slower growth in transfers, and potentially fewer (e.g. program eliminatinos) or lower service levels (e.g., processing times, enforcement, infrastructure maintenance). In macro terms, cuts are deflationary, they reduce aggregate demand, which can cool inflation but also growth and employment in the short run.

Tax increases: Higher effective tax rates reduce disposable income and/or after-tax returns to investment, is also deflationary. Design matters: broadening the base (fewer exemptions) generally distorts behavior less than steep marginal rate hikes, but either path tightens demand.

Because both mechanisms have a contractionary/deflationary impact and create conditions that can lead to recession, economic hardship, and job loss, a multi-year consolidation approach is part of Dalio’s framework. Instead of a fiscal cliff and extreme austerity based spending cuts; Dalio’s approach phases changes over time; and pairs tighter budgets with growth-friendly policies (innovation, expansion, permitting, skills, productivity increases) that lift the supply side. The goal is to keep nominal GDP growth (real growth + inflation) from collapsing, otherwise debt-to-GDP can rise even while you cut, because the revenue denominator shrinks.

Deleveraging Menu (and Their Trade-offs)

The Tax Project has outlined (See our Article: “Ways Out of Debt”) a non-exhaustive review of policy options to deleverage. Below we provide a summary group them by mechanism. [10]

1) Consolidation via Revenues (Tax Increases)

Summary: Revenue measures (Tax Increases) are deflationary near-term but can be structured to minimize growth drag (e.g., emphasize consumption/external taxes with offsets, or reduce narrow, low-value tax expenditures).

2) Consolidation via Outlays (Spending Cuts)

Summary: Spending cuts can be deflationary; pairing it with supply-side reforms (education/skills, streamlined permitting for productive investment, R&D incentives, labor force productivity growth) can mitigate growth losses and raise potential output over time.

3) Pro-Growth, Supply-Side Reforms (Growth)

Summary: Growth and Supply side reforms (e.g. Productivity, Innovation, Permitting, Energy inputs) that generate real productive growth is the least painful way to lower debt-to-GDP without relying on high inflation.

4) Inflation and Financial Repression (Print Money)

Summary: Modest inflation can ease real debt burdens, part of Dalio’s balance, while managing highly destructive excess inflation. That is why the “beautiful” approach uses only modest inflation alongside real growth, fiscal and monetary management, not inflation as the main lever. [7][9]

The Sooner we Start, the Easier it is

The bottom line is, the longer we wait the harder it gets, the problem will not go away on its own, it only gets worse over time. The 2025 CBO long-term outlook provides a forecast, and it doesn’t paint a great picture:

Debt Outlook: Debt held by the public rises toward 156% of GDP by 2055, under current-law assumptions. [8][11]

Outlays vs Revenues: Outlays (spending) climbs from ~23.7% of GDP (2024) to 26.6% (2055); revenues rise more slowly to 19.3% – expanding an already large and persistent structural gap. [8][12]

Net interest: Reaches 5.4% of GDP by 2055—roughly one-fifth of total federal outlays and around 28% of Federal revenues. [7][8][9]

Those numbers underscore the reason to start now: the later the adjustment, the harder the challenge required to stabilize debt. Conversely, a timely package that the public views as credible and fair can anchor long-term rates lower than otherwise, reducing the interest burden mechanically.

A “Beautiful” U.S. Deleveraging

The Tax Project does not propose or advocate specific policies, however a workable plan using the Dalio Framework would likely include a mix of the following components aimed to stabilize debt-to-GDP within a decade and then bend it downward while sustaining growth and guarding against excessive inflation relapse. A balanced approach:

A multi-year fiscal framework enacted up front allowing for a ordered and measured deleveraging.

Credible guardrails: Deficit targets linked to the cycle; a primary-balance path that improves gradually, with automatic triggers to correct slippage.

Composition: Roughly balanced between base-broadening revenues and spending growth moderation in the largest programs (phased in).

Quality: Protect high-return public investment; target lower-value spending and tax expenditures first.

Administration: Resource the revenue authority to improve compliance; align incentives and simplify.

A growth package to offset the deflationary impulse.

Supply-side reforms with high ROI: energy and infrastructure permitting; skilled immigration; workforce skills; competition policy that fosters innovation and productivity tools.

Private-sector: Reduce regulatory frictions that impede capex expenditures in goods and critical infrastructure.

Monetary-Fiscal Coordination in the background—not Fiscal Dominance.

Monetary-Fiscal Coordination: The Federal Reserve keeps inflation expectations anchored; it does not finance deficits but it can smooth the adjustment by responding to the real economy and anchoring medium-term inflation near target. Over time, a credible Fiscal policy promoting growth helps bring Rates (R) down toward Growth (G), easing the arithmetic. [7][9]

Contingency tools (use sparingly)

“Terming out” Treasury debt Lock in more fixed, long-term loans and rely a bit less on short-term IOUs. Why it helps: If rates rise, less of the debt has to be refinanced right away, so interest costs don’t spike as fast. If the term premium is reasonable and the Fed is in an accommodative stance, shorter term lower rate treasuries maybe attractive to reduce Net Interest expenses.

Targeted restructuring (not the federal debt—specific borrower groups) Adjust terms for groups where relief prevents bigger damage (e.g., income-based student loan payments, disaster-area mortgage deferrals). Why it helps: Stops small problems from snowballing into defaults and job losses while the government tightens its own budget.

This mix qualifies as “beautiful” by balanacing inflationary and deflationary elements. It shares the burden across levers; it avoids hard financial shocks; it relies primarily on real growth + structural balance rather than high inflation or sudden austerity. Done credibly, long-term rates fall relative to a laissez-faire (do nothing) approach, lowering interest costs directly and via lower risk premia. The country benefits both intermediate (by not inducing a recession and harsh economic measures), and long term freeing up revenue to more productive uses than Debt payments, and supporting growth.

Managing the Macro Balance: Deflation vs Inflation

All this sounds good, but the practical art is to offset deflationary consolidation with pro-growth supply measures, not with high inflation. Consider the balancing act between these different variables:

Consolidation (deflationary): Fiscal discipline reduces demand, manages structural gaps, good for taming inflation; risky for growth if overdone or badly timed.

Growth Reforms (disinflationary over time): Expand supply, lower structural inflation pressure; raise real GDP and productivity, improving the debt to GDP ratio.

Monetary Stance: Should keep inflation expectations managed; if growth softens too much, gradual monetary easing is available if inflation is on target.

Inflation temptation: Modest inflation can reduce some of the burden mechanically, but leaning on inflation as the adjustment tool can backfire if markets demand higher interest rate (term) premiums; nominal rates can rise more than inflation, worsening R > G and Net interest. CBO’s baseline already shows interest outlays rising markedly even without an inflationary strategy. [7][9]

A “Beautiful Deleveraging“ aims too creates a “soft landing” keeping nominal GDP growth positive, inflation expectations managed, and real growth strong enough that debt-to-GDP falls without creating undue Economic hardships. Managing each of these variables with the often blunt tools available, many of which don’t manifest for months, or years is quite the magic trick, requiring patience, skill, and acumen.

Risks and Pitfalls

The road ahead can be bumpy and full of challenges, managing the risks is key to a successful deleveraging. Here are some areas that can derail a “Beautiful Deleveraging.”

Front-loaded austerity that slams demand into a downturn or recession; a gradual path anchored by rules and automatic stabilizers is safer and creates less hardships. It means that we will endure less pain over a longer period. Some may want to rip the band aid off and take the measures all at once.

Policy whiplash (frequent reversals) that destroys credibility and raises risk premia (higher Interest rates); stable consistent policies beat one-off “grand bargains” and political vacillations.

Over-reliance on rosy outlooks; plans should make conservative growth assumptions, and reasonable baselines.

“Kicking the can” down the road with laissez-faire policies until interest dominates the budget, leaving painful, crisis-style adjustments as the only option is the biggest of all the Risks. CBO’s outlooks illustrates how waiting raises the eventual cost, and negative consequences. [7][8][9]

Is it Worth it?

On the surface, that’s an easy question, however the answer may pit generations against each other each with their own point of view and different perspectives. Current generations at or near retirement who may not see the worst effects of a laissez-faire policy may see the risk of recession, and cut backs in service as an unacceptable change to their Social Contract which they may have worked a lifetime under a set of expectations that they counted on. Younger generations, may see it as generational theft, placing an undue burden on them for debt they had little or no part in creating. Both are valid perspectives, however, the long term effects of a “Beautiful Deleveraging” will deliver these positive durable payoffs for the Country:

Out of Doom Loop: High debt is a trap, as out of control interest expenses rise, debt grows and the gap between revenue and debt rises in a self reinforcing doom loop. Breaking that loop is key to a healthy economy.

Lower Interest burden: As debt drops, so does Net Interest expenses. Instead of crowding out other expenses, revenue is freed up to other National Priorities (e.g. Healthcare, Education, Infrastructure, Social Services, Surplus, Sovereign Wealth). [7][9]

Greater Macro resilience: With manageable debt exogenic shocks, pandemics, wars, financial events, give the Government financial space to manage these events without taking on negative levels of debt.

Higher Trend growth: When consolidation is paired with genuine productivity reforms, lower debt ratios are correlated with higher growth, supporting living standards and the tax base. [14][15][16]

Summary

A “Beautiful Deleveraging” is but one way to approach the intractable problem of high debt. It represents a reasonable approach that balances near term realities with long term impacts. Our choices now will define the America of the future, and the quality of life younger Americans will have and future generations will inherit. Will it be painless? Probably not, it will likely require some sacrifice and discipline. The challenge wasn’t created in a short period, and it won’t be solved in a short period. Is it achievable? If we face the truth with candor about trade-offs, accept phased steps that the public deems fair, and have a bias toward investments that raise long-term productive capacity, than it is possible. The biggest question is the will of the American people. That, more than any single policy, will determine our future. At the Tax Project we will always bet on informed Citizens making the best choices for America – we will always bet on America. That defines the essence of a “Beautiful Deleveraging.” [3][4][10]

Citations

[1] U.S. Department of the Treasury, America’s Finance Guide: National Debt (accessed Oct. 2025): “The federal government currently has $37.98 trillion in federal debt.” (fiscaldata.treasury.gov)

[2] Joint Economic Committee (JEC) Debt Dashboard (as of Oct. 3, 2025): Gross debt ~$37.85T; public ~$30.28T; intragovernmental ~$7.57T. (jec.senate.gov)

[3] Ray Dalio, What Is a “Beautiful Deleveraging?” (video explainer). (youtube.com)

[4] Ray Dalio, short-form clip on “beautiful deleveraging.” (youtube.com)

[5] Reuters coverage of CBO near-term deficit path (FY2024-2025). (reuters.com)

[6] Associated Press summary of CBO’s 10-year outlook (debt +$23.9T over decade; drivers). (apnews.com)

[7] Congressional Budget Office, The Long-Term Budget Outlook: 2025 to 2055—headline results: net interest 5.4% of GDP by 2055; outlays path. (cbo.gov)

[8] Peter G. Peterson Foundation, summary of the 2025 Long-Term Outlook: outlays to 26.6% of GDP; interest path and historical context. (pgpf.org)

[9] Committee for a Responsible Federal Budget (CRFB), analysis of CBO 2025 outlook: interest consumes ~28% of revenues by 2055; R > G later in the horizon. (crfb.org)

[10] Tax Project Institute, Ways Out of Debt: US Options for National Debt (June 14, 2025). (taxproject.org)

[11] Reuters recap of CBO long-term debt ratio (public debt ~156% of GDP by 2055). (reuters.com)

[12] CBO, Budget and Economic Outlook: 2025 to 2035 (context for near-term path). (cbo.gov)

[15] Cecchetti, S. G., Mohanty, M. S., & Zampolli, F. (2011). The Real Effects of Debt (BIS Working Paper No. 352). Bank for International Settlements.

[16] Eberhardt, M., & Presbitero, A. F. (2015). Public debt and growth: Heterogeneity and non-linearity. Journal of International Economics, 97(1), 45-58.

The United States in the mid-1940s, the country had just financed the most expensive and bloody war in history. Something new is occurring: paychecks for the first time begin withholding income tax out of those paychecks as they are earned. The so called “Gold Standard” where Gold backs every dollar as a legal promise is gone for Americans. The Federal Reserve is learning how to steer interest rates for a peacetime economy. Beardsley Ruml, a former Macy’s finance chief turned New York Federal Reserve chair steps into this backdrop and writes an article in the January 1946 American Affairs publication with a simple but provocative statement:

“Taxes for revenue are obsolete.”

Beardsley Ruml

He isn’t trolling – he meant what he said. He’s telling readers that the way money works has changed, and if we keep thinking about Federal taxes like a family checking account, “first earn, then spend”, we misunderstand how money works in a fiat currency not backed by a hard asset (like gold) and what taxes actually do in a monetary system. The government no longer needs to wait for tax revenue to spend. Stop for a second and think about this statement, it is a Matrix like moment where Morpheus asks Neo if he wants the Red Pill or the Blue Pill. The Red Pill represents the truth and how fiat currency actually works, and the Blue Pill represents just ignoring the truth and going back to your comfortable understanding of how money works. A full copy of Ruml’s Thesis can be found here.

Fiat currency is money that is not backed by a physical commodity like gold or silver, but is instead backed by the government that issued it. Its value comes from the public’s trust and the government’s authority, which decrees it as legal tender. Examples of fiat currency include the U.S. Dollar, the European Union’s Euro, and the Japanese yen.

The Backdrop for Ruml’s Thesis

When Beardsley Ruml wrote “Taxes for Revenue Are Obsolete,” he was synthesizing his experiences of how American money actually worked, and the changes going on around him. As a Federal Reserve chair, participant in Bretton Woods, and someone who shaped policy, like Pay as you go payroll, he had a first hand view.

1933–1934: Off domestic gold—constraint shifts inside the border

In the early New Deal years, the U.S. ended domestic gold convertibility and reorganized the gold regime under the Gold Reserve Act. Inside the country, dollars were no longer legally IOUs for a fixed weight of metal. The binding constraint on federal finance began to migrate from gold reserves to inflation, real capacity, and statute (law). Ruml’s essay explicitly ties his thesis to this inconvertible-currency reality: a national state “with a central banking system… [whose] currency is not convertible into any commodity.” [1]

“Final freedom from the domestic money market exists… where [there is] a modern central bank, and [the] currency is… not convertible into gold.” [1]

1942–1943: Pay-as-you-go withholding—taxes become continuous

With wartime employment booming, Ruml helped push paycheck withholding (the Current Tax Payment Act of 1943), turning the income tax from an April settlement into a real-time flow. Withholding didn’t just improve administration; it made taxes a live instrument for managing purchasing power across the year, reinforcing Ruml’s view that taxes should be judged by effects—on prices, distribution, and behavior rather than as a cash bucket to “fund” future outlays (spending). [5]

1944–1946: Bretton Woods and the New York Fed vantage point

As Bretton Woods took shape (par exchange rates, gold convertibility for foreign official holders, capital controls), Ruml was chairman of the New York Fed (wartime through 1946). He watched the Fed support Treasury borrowing for war finance and then toward peacetime normalization. In that setting, Ruml saw operationally how Treasury spending settled through the Federal Reserve, and how taxes and bond sales later lowered purchasing power and supported interest-rate control. He previewed his thesis in a 1945 address and then published the 1946 essay, sharpening the claim that taxes are essential for what they do, not to generate revenue before spending. [1]

“All federal taxes must meet the test of public policy and practical effect.” [1]

1951: The Treasury–Fed Accord—roles clarified

Ruml’s essay was given before the Treasury–Fed Accord, but the Accord (1951) confirmed the institutional direction he was pointing toward: monetary-policy independence to target rates and prices, separate from Treasury’s debt-management imperatives. After pegging wartime yields, the Fed reclaimed the ability to resist fiscal pressure when inflation called for tighter settings—strengthening the case that budgets should be judged by employment, prices, and distribution, not balanced-budget rituals. [3]

Ruml died in 1960, but his logic became even more straightforward after Nixon suspended official dollar–gold convertibility and major currencies moved to floating exchange rates. From then on, the United States was unambiguously a fiat-currency issuer: spending cleared through the Fed first; taxes and bond sales followed to manage inflation, distribution, market structure, and interest rates. Ruml’s once-provocative line read less like heresy and more like a plain description of operations—with the real constraints now fully on inflation, capacity, and institutional credibility. [4]

“The public purpose… should never be obscured in a tax program under the mask of raising revenue.” [1]

So the events and experiences: moving internally away from gold backed assets at home (1933–34), real-time taxation (1943), Fed Monetary Autonomy (1951), and externally away from gold (1971–73) together explain how Ruml could say, without gimmicks, that taxes are essential for what they do: price stability, distribution, behavior, and currency demand—rather than as a prerequisite to spend. He believed the question for any program was:Can the real economy deliver, and how will policy manage the price-and-capacity path along the way?[1][3][4][5]

Follow the dollar: how “mark-up” works

To see understand Ruml’s Thesis more concretely, we can use by example a single payment.

A federal contractor finishes a bridge repair job. Treasury authorizes payment to the contractor. The Federal Reserve, which is the government’s bank, marks up the contractor’s checking account at their commercial bank. Two things happen at once:

The contractor’s deposit goes up (their balance goes up, they have more spendable money).

The contractor’s commercial bank’s reserve balance at the Fed goes up (the bank’s settlement cash).

No one at the IRS had to collect that exact amount yesterday for this payment to clear today. In other words, the government did not have to wait for revenue before spending. The payment clears because the United States operates the dollar system. Once that payment is made, taxes later can remove some of those dollars from private hands; and bond sales can swap some deposits/reserves for Treasury securities to help the Fed keep interest rates where it wants them.

That’s the basics of Ruml’s claim. In a fiat system with a central bank, spending isn’t bottlenecked by prior tax receipts. The real limits are inflation and real capacity – how many workers, machines, homes, kilowatts, and microchips the economy actually has.

“Federal taxes can be made to serve four principal purposes…” [1]

Ruml’s Four Functions for federal taxes then are as follows:

Price stability (control inflation by removing purchasing power when the economy runs hot)

Distribution (redistributing wealth (purchasing power) based on policy)

Behavior/structure (altering behavior with economic incentives e.g. carbon, tobacco, alcohol, etc.)

Currency demand/legitimacy (creating demand for currency by requiring Federal taxes be paid in Dollars)

Questions from Ruml’s thesis

Not only was Ruml’s thesis provocative, if true it brings up a whole set of new questions, and challenges a lot of our notions of money and taxes.

Question: If spending can come before tax revenue, and the government doesn’t need it to spend, why are we paying taxes at all? This is the heart of Ruml’s Thesis, that while the government did not need taxes to allow the government funding to spend, taxes did play an important role. Ruml believed taxes were a way to manage price stability (inflation): they help keep prices in check by reducing purchasing power (demand), they shape who holds purchasing power, and they anchor the currency by requiring dollars to settle tax bills. Without taxes, you could spend for a time but you would lose price stability and the public’s confidence in the stability of the dollar itself.

Question: Why do politicians still ask “How will you pay for it?” if taxes aren’t needed to spend? Because you hit walls long before you “run out of money”:

You can’t print money for Imports. If spending weakens the value of the dollar, import prices jump or supplies dry up. That impacts living standards fast. [18][19][20]

Boom–bust finance. Prolonged easy fiscal + easy money can inflate asset and credit bubbles; when they pop, banks retrench and recessions deepen—costlier than using modest drains (purchasing power reductions) earlier. [9]

Tax-base erosion (seigniorage limit). If people expect rising prices and weak policy response, they flee into hard assets/FX; real tax intake falls just when control is needed (seen in hyperinflations). [16][17]

Real-world choke points. Money doesn’t increase productivity, create nurses, build cars, ports, or grid lines; increasing demand into bottlenecks yields price instability, not output. [10][12][13][14]

Interest-cost feedback. Rate hikes to cool inflation raise government interest bills, shifting income toward bondholders and forcing tougher trade-offs later. [11][9]

Predictable Policy keep costs low. Predictable authorizing/phase-out rules lower risk and support long-term contracts; junk the rules and borrowing costs/investment worsen even before inflation moves. [11][9]

Ruml’s point isn’t spend in excess, it’s that taxes aren’t required to spend. Taxes and pacing are the governors that keep prices stable, protect access to vital imports, prevent financial bubbles, and align demand with what the real economy can actually deliver. [1][2][3][6][7]

Question: Why not just make everyone a billionaire? This is an interesting thought exercise, if everyone was a billionaire would the purchasing power of the currency be the same? Since money is a claim on real output, not actual output (productivity) if everyone was a billionaire most certainly the purchasing power of the fiat currency would be substantially lower. More money without more productivity (nurses, houses, energy, widgets, etc.) brings higher prices (inflation), not greater prosperity. Ruml’s thesis keeps taxes (and other monetary mechanisms to reduce purchasing power) in the toolkit precisely to match purchasing power to capacity.

Japan: Use Case and cautionary tale

Japan is the cleanest real-world test of part of Ruml’s thesis. For decades, Japan’s gross public debt sat well above 200% of GDP—yet long-term interest rates were near zero under Bank of Japan (BOJ) policy. The Yen has had no solvency crisis, of major uncontrolled inflation. That supports Ruml’s point that a nation which issues debt in its own currency faces inflation and capacity constraints more than a “running out of money” constraint [12][13].

However, during the same period shows why Ruml’s mechanics don’t solve the growth problem by themselves:

The “lost decades.” Japan endured a multi decade stretch of weak real growth and disinflation/deflation. Even with easy financing conditions Japan was not able to create growth and productivity improvements or new sectors on their own [14][16].

Balance-sheet hangover. After the 1990s asset bust, households and firms deleveraged for years—private demand stayed weak even when public deficits filled part of the gap.

Wages and demographics. An aging population, shrinking workforce, and corporate practices contributed to sluggish productivity and flat real wages for many workers [14][16].

Foreign Exchange (FX) and imported prices. Episodes of yen weakness raised import costs (notably energy), squeezing households and complicating the path out of very low inflation.

Policy evolution. The BOJ cycled through low rates including zero and even negative interest rates for 8 years!, Quantitative Easing, and yield-curve control, then gradual adjustments. These tools stabilized finance but didn’t create robust growth, reminding us that supply-side capacity (energy, housing, innovation, corporate reform) still determines living standards.

Monetary sovereignty may avoid immediate solvency issues in your own currency, but prosperity still depends on productivity, demographics, and the supply side. The policy art isn’t printing more money; it’s about managing the balance between demand and capacity so money meets output rather than outruns it. [12][14][16]

Where Ruml’s Thesis fails

Ruml presumes monetary sovereignty – you tax and spend in your own currency, with credible institutions, and you don’t owe large amounts in someone else’s money, or require external inputs like energy, food, or other goods and raw materials. It also assumes you don’t outspend the productive capacity of the country. If and when those conditions vanish, significant and detrimental impacts could fall upon the country. There are a number of examples of hyper inflation, that have damaged the economic and well being of countries.

Weimar Republic Germany (1921–23). Huge reparation obligations (external), political fracture, and aggressive central-bank financing into a collapsing anchor produced hyperinflation. The issue wasn’t “deficits” in the abstract; it was external liabilities + institutional breakdown + supply dislocation [18].

Zimbabwe (2000s). Radical output collapse (agriculture and supply chains), governance failures, and money creation against shrinking real capacity drove prices into hyperinflation. Too many nominal claims, too little real output [19].

Sri Lanka (2022). A foreign-currency crisis: depleted FX reserves, weak tax base, and large hard-currency debts. You cannot print your own fiat money when your liabilities are in dollars/euros; the constraint becomes imports and external financing, not domestic “solvency” [20][21][22].

Ruml’s Thesis exists when you issue your own currency, are not dependent on externalities or foreign debt, and spending does not outpace productive capacity and credibility in currency is maintained. Lose those – and inflation, devaluation, and/or default can take the driver’s seat.

How most Economists think about Ruml’s Thesis

Most modern economists agree on the operational basics: in a fiat currency system, the Treasury and central bank can ensure payments clear in the home currency; taxes/bonds then drain purchasing power and help the central bank hit an interest-rate target. That’s not controversial [6].

Where Economists caution starts – real life, not the textbook:

Prices can jump if demand outruns supply. If new spending hits an economy short on cars, nurses, chips, or houses, prices rise. That happened in 2020–22 during the COVID Pandemic: demand recovered while supply was jammed. Changing taxes or budgets is slow, so economists like built-in brakes (automatic stabilizers) and phased rollouts. [6][7][2]

Higher interest rates make debt cost more. The U.S. can always pay in dollars, but when the Fed hikes to fight inflation, the interest bill on government debt climbs. If that bill grows faster than the economy or tax revenue, Congress faces tougher trade-offs. Last year Net Interest on the US National Debt was over $1 trillion. The 1951 Accord exists so the Fed can fight inflation even if it makes borrowing costlier. [3][10][11]

Consumer Sentiment and Beliefs matter. Prices stay more stable when people trust leaders will cool inflation off if needed. If policy looks like “spend without limits,” businesses and workers build in higher inflation into their cost models and pass that along, and it’s harder to bring back down once its gone up.

Not every side effect shows up in the Consumer Price Index (CPI). Inflation can manifest itself in many ways that trickle down to the ordinary consumer in ways that aren’t tracked well by major indexes like the CPI. Big deficits with low rates can push up stock and house prices and widen wealth gaps, even if everyday inflation isn’t high. That can erode support for useful programs. [10]

At full tilt, something has to give. When the economy is already near full capacity, more public spending creates demand that competes with private demand for the same workers, resources, and materials. The result isn’t “no money”; it’s higher prices or shifting resources away from something else. This can be managed with taxes destroying demand, phased timing reducing demand peaks, or adding supply.

America, and most countries are deeply intwined in Global Trade We import energy, food, critical resources, and key parts from a Global Supply chain. If the dollar weakens or suppliers get nervous, import prices rise and shortages can appear. Building domestic capacity (energy, logistics, housing) and self sufficiency can offset that, but it also comes at a cost.

Where Economists actually stand on Ruml’s thesis

Broad agreement on the plumbing: Most economists accept that in a fiat system the government can pay first in its own currency, and that taxes/bonds are tools to manage demand and interest rates. That’s mainstream (see the Bank of England explainer). [6][7]

Support for using deficits in slumps: In recessions or emergencies, many economists favor deficit spending to protect jobs and speed recovery. (Ruml’s taxes aren’t required for spending fits this.) [6][7]

Caution about pushing it too far: Many are wary of treating “spend first” as a green light without a clear plan for inflation, ensuring demand doesn’t outpace supply and productive capacity, and the outside world (Global trade, key economic inputs from outside the U.S.). They stress guardrails, automatic stabilizers, and credible roles for the Fed and Congress (the spirit of the 1951 Accord). [3][10][11]

Split on the stronger claims (often linked to MMT):

Critics say relying mainly on taxes to stop inflation is too slow and political, and they worry about fiscal dominance (pressuring the Fed to accommodate debt). They also flag open-economy risks and asset-price side effects. [9]

Supporters respond that good design (automatic tax/benefit adjusters, phasing, targeted drains) can handle those issues, and that recognizing the fiat mechanics helps us focus on real limits (people, machines, energy) rather than imaginary cash limits. [9]

Economist View Summary:

They mostly agree on the mechanics.

They agree deficits can be useful tools.

They differ on how far you can push spending before you risk inflation, financial stress, or FX problems

They differ on whether taxes can be used quickly and fairly enough to cool inflation off. [6][7][3][10][11][9]

A Ruml-style way to judge any Spending program

The Congressional Budget Office estimates the cost and budget impact of programs. Using a Ruml Thesis style way to evaluate programs might look something like this.

Capacity: Do we have the people, skills, materials, energy, and productive capacity? If not, what’s the plan to expand supply?

Inflation plan: If demand overheats, what automatic brakes kick in—phasing, adjustable credits, temporary surtaxes? [2]

Distribution: Who gets the new purchasing power and who gives something up?

External exposure: Are we import or FX sensitive in the relevant inputs? Do we hold external exposures?

Institutional alignment: Are fiscal choices made with a central bank focused on price stability (the post-1951 lesson)? [3]

Summary: Ruml’s answer to the question

In summary we ask the title question: “Are taxes needed,?” Ruml’s answer—in his own words—is that their revenue role is not the point in a fiat system:

“Taxes for revenue are obsolete.” [1]

They are needed for what they do: to keep prices stable, shape distribution and behavior, and anchor demand for the dollar:

“Federal taxes can be made to serve four principal purposes…” [1]

And the standard for judging them is not myth or ritual but outcomes:

“All federal taxes must meet the test of public policy and practical effect.” [1]

Read that together and you have the summary of his thesis: the United States does not tax so that it can spend; it taxes so that the money it spends produces stable prices, fair distribution, incent certain behaviors, and ensure a credible currency. While his beliefs were provocative at the time, and still controversial, the mechanics of his thesis remain true and you can see his influences in the roots of Neo Chartalism, Functional Finance and all the way to Modern Monetary Theory (MMT) today.

The “Debasement Trade” is a prominent investment strategy in current finance, defined by the systematic movement of capital out of assets denominated by sovereign promises, such as fiat currencies and traditional fixed-income securities, and into assets characterized by verifiable, finite supply, often referred to as “hard assets” [1]. This strategy is fundamentally a defensive measure, designed to preserve the real value of wealth against the risk of the currency’s diminishing purchasing power, which results from accelerating national debt and large/rapid monetary expansion [2]. The shift reflects a growing, fundamental loss of confidence in the long-term fiscal solvency of major economies, especially the United States, whose currency serves as the global reserve.

I. Historical Context: Debasement as a Sovereign Tool

The act of currency debasement, the reduction of a currency’s intrinsic value without altering its face value, has been a recurring fiscal strategy throughout history. While the methods have evolved, the economic rationale remains consistent: to increase the effective money supply to meet government financial needs, typically to fund large expenditures or manage mounting debts [3].

Physical Debasement: The Precedent

In the ancient and medieval worlds, debasement was a physical process. The Roman Empire offers a classic example, where successive emperors reduced the silver content of the denarius over several centuries [4]. By substituting precious metals with cheaper base alloys, the government could mint a greater volume of currency from the same reserves, allowing the Treasury to stretch its resources for state expenses. This practice, however, led directly to rising prices (inflation) as merchants recognized the coin’s diminished intrinsic worth.

Another significant example occurred in 16th-century England under King Henry VIII, a period often cited as the “Great Debasement” [5]. To finance ongoing conflicts, the silver purity of English coinage was drastically reduced (From over 90% to as low as 25%). This act, while providing short-term funding for the Crown, destabilized domestic and international trade, leading to public mistrust and prompting the widespread hoarding of older, purer coins—an economic phenomenon later formalized as Gresham’s Law (“bad money drives out good”) [5].

The Structural Shift to Fiat Debasement

The transition to a fiat monetary system fundamentally redefined debasement. Following President Nixon’s 1971 decision to suspend the convertibility of the U.S. dollar into gold, the global financial system moved entirely away from the commodity-backed anchors of the Bretton Woods agreement [6] (See our Article on Bretton Woods). In this modern context, debasement is not about physical manipulation but about administrative action: the unconstrained expansion of the money supply through central bank policy. The erosion of a currency’s value is now primarily a function of excessive issuance relative to underlying economic productivity [7].

US M2 Money Supply

Figure 1 Source: Federal Reserve

II. The Conditions of the Modern Debasement Trade

The current period is characterized by macroeconomic conditions that have accelerated investor concern and institutionalized the Debasement Trade as a key portfolio consideration.

The Scale of Sovereign Indebtedness

The primary catalyst is the unprecedented scale of the U.S. National Debt, which is over $37 trillion [8]. Unlike previous debt cycles, the current trajectory is sustained by structural spending (23 consecutive years with deficit, last 5 $trillion+), regardless of the political party in power [9]. This fiscal reality presents governments with a limited set of options: implement politically unpalatable spending cuts or tax hikes, or employ the politically more palatable solution of allowing the currency’s value to decline.

The Debasement Trade is predicated on the rational assumption that policymakers will inevitably choose the latter, utilizing monetary tools to reduce the real burden of the debt and its service costs [1]. Through inflation, the real value of the debt owed to bondholders is effectively diminished over time, a process often described as “financial repression.”

Investor Flight to Scarcity

The response from institutional investors has been explicit. Citadel CEO Ken Griffin has been a vocal proponent of this thesis, characterizing the current market environment as a “debasement trade” [10]. Griffin notes a tangible shift in capital, with investors seeking to “de-dollarize” and “de-risk their portfolios vis-a-vis US sovereign risk” by accumulating non-fiat assets [10].

This trend is observable through market data:

Currency Depreciation: The U.S. dollar index (DXY) has experienced significant periods of sharp depreciation against major currencies and, more dramatically, against hard assets like gold [11].

Reserve Diversification: Globally, the dollar’s share as the primary reserve currency held by central banks has been steadily declining, reaching multi-decade lows [12]. This signals a structural move by foreign governments to reduce reliance on the U.S. dollar, further supporting the debasement thesis [13].

US Dollar Valuation

Figure 2 Source: Federal Reserve

III. Monetary Policy, QE, and Hyper-Liquidity

The mechanics of modern debasement are inextricably linked to central bank interventions, specifically Quantitative Easing (QE).

Quantitative Easing and Money Supply Growth

QE, a policy initiated following the 2008 Financial Crisis and dramatically expanded during the 2020 COVID pandemic response, involves the central bank (the Federal Reserve) creating new electronic money to purchase vast amounts of government and mortgage bonds [14]. This injects large amounts of money (hyper-liquidity) into the financial system, resulting in an exponential, historically unprecedented surge in the M2 money supply (See Figure 1) [14].

This expansion is the engine of modern debasement. When the volume of money in circulation grows at a pace far exceeding the underlying growth in the economy’s productive capacity, the result is an inevitable loss of the currency’s value [15].

Inflation as the Mechanism of Debasement

The consequence of this imbalance is widespread inflation, which acts as the functional manifestation of currency debasement. Inflation is not merely a rise in prices but a measurable loss of the currency’s ability to retain its value [15]. Some consider this type of inflation a hidden tax (See our Article on Is Inflation a Stealth Tax?). Data confirms this erosion: significant cumulative price increases over recent five-year periods have fundamentally lowered the purchasing power of the dollar [10].

The Debasement Trade views inflation as structural rather than temporary—a direct result of governments financing massive deficits through the printing press, effectively taxing the population through reduced purchasing power rather than legislative mandate.

US Inflation

Figure 3 Source: Federal Reserve

IV. Political Debate and the Precedent of the Plaza Accord

The current anxiety surrounding debasement is focused on specific policy discussions within Washington concerning the intentional manipulation of the dollar’s value.

The Deliberate Devaluation Thesis

Certain U.S. economic advisors, notably within the Trump administration, have argued that the dollar’s status as the world’s reserve currency creates a structural “overvaluation” that persistently harms U.S. trade competitiveness [16]. Proponents of this view suggest that managing a controlled depreciation of the dollar is a necessary measure to correct global trade imbalances and support domestic manufacturing [16].

This thesis has led to policy suggestions, sometimes grouped conceptually under the name “Mar-a-Lago Accord.” These suggestions include strategies such as utilizing tariffs to adjust global currency levels or even taxing foreign holders of U.S. Treasury debt [16]. Such discussions signal a willingness by policymakers to consider actions to achieve fiscal and trade goals, even at the expense of currency stability (Inflation).

Purpose: The Plaza Accord was a multilateral agreement signed by the G5 nations (France, West Germany, Japan, the United Kingdom, and the United States) [17]. Its specific goal was to engineer an orderly depreciation of the U.S. dollar against the Japanese yen and German Deutsche Mark. At the time, the U.S. dollar was considered significantly overvalued due to high U.S. interest rates and robust capital inflows, which led to a massive U.S. trade deficit [18].

Mechanism: The participating nations agreed to coordinate currency market interventions, specifically selling U.S. dollars, to achieve the desired depreciation [18].

Outcome and Relevance: The Accord successfully achieved its short-term goal, weakening the dollar significantly [18]. However, it ultimately failed to deliver long-lasting correction to the underlying U.S. trade imbalances because the structural domestic factors—namely, low private savings and high government borrowing—remained unaddressed [19].

The historical parallel is crucial: while a new “accord” might temporarily achieve a devaluation target, the Debasement Trade argument suggests that without fundamental fiscal discipline, any managed decline will merely lead to renewed instability and require further monetary interventions.

The Official Stance

Despite the policy discussions, U.S. Treasury Secretary Scott Bessent has publicly distinguished between short-term currency fluctuations and long-term policy [20]. He maintains that the core of the U.S. “strong dollar policy” is to take long-term steps to ensure the dollar remains the world’s reserve currency, focusing on U.S. economic growth and stability, rather than obsessing over the exchange rate [20]. This distinction is intended to reassure global markets that the U.S. is not actively pursuing the dollar’s demise, even if domestic fiscal and monetary choices suggest otherwise.

V. Implications for Citizens and the Move to Hard Assets

The consequences of currency debasement are most keenly felt by the average citizen, whose financial well being may depend on the dollar’s stability. This is especially true after the post COVID rapid inflation period felt by most Americans who are now keenly aware of the negative impacts of inflation.

Inflationary Wealth Transfer

Debasement operates as a stealthy wealth transfer mechanism [21].

Erosion of Fixed Income: Citizens holding dollar-denominated assets, such as savings accounts, fixed pensions, and bonds, see the real value of their wealth diminish steadily [7]. This is especially punitive for retirees and those on fixed incomes.

Asset Price Distortion: While nominal asset prices (stocks, real estate) reach record highs in dollar terms, this surge is often an illusion. When these assets are measured against hard assets like Gold or Bitcoin, the appreciation is significantly tempered, reflecting the currency’s dilution rather than pure economic growth [22].

This disparity: those who are asset-rich (owners of real estate, commodities, or equities) are protected, while the working class and cash holders are negatively effected as their wages and savings buy less in real terms.

The Embrace of Hard Assets

The Debasement Trade is the strategic answer to this inflationary trap. Investors are choosing assets defined by their scarcity:

Gold (Traditional Hedge): Gold has served as a reliable store of value and inflationary hedge for millennia, its value enduring precisely because it cannot be created by a central bank [23]. Surges in the gold prices directly reflect the decline in the dollar’s relative value [12].

Bitcoin (Digital Scarcity): Bitcoin has been increasingly adopted as a contemporary hard asset [1]. Its maximum supply of 21 million coins is secured by cryptography and network consensus, rendering it immune to sovereign fiscal or monetary manipulation [2]. Its inclusion in the Debasement Trade reflects a redefinition of “hard money,” moving beyond the physical limitations of precious metals to the mathematical certainty of code [22]. The dramatic appreciation of Bitcoin is viewed by many investors not as a speculative frenzy, but as a rational re-pricing of mathematical scarcity relative to infinitely expanding fiat currency [1].

USD vs Hard Assets

Figure 4 Source: TradeView

VI. Conclusion: A Structural Shift

The Debasement Trade is more than a momentary market tactic; it is a structural investment shift reflecting deep seated concerns over fiscal integrity of the world’s leading economies. Driven by high and persistent debt accumulation, coupled with the unconstrained power of central banks to expand the money supply through QE, the trade represents a fundamental shift in investor trust, from faith in government promises to reliance on the verifiable scarcity of hard assets. As long as the structural imbalance between monetary creation and productive capacity persists, the strategic movement toward assets like gold and Bitcoin will continue to be a defining feature of the global financial landscape.

Webull (syndicated from Bloomberg/Benzinga). (2025, July 3). U.S. Treasury Secretary Bessent refuted claims that the recent depreciation of the U.S. dollar would affect its status as the world’s major currency. https://www.webull.com/news/13098149616067584 (Webull)

Tax Project Institute is a fiscally sponsored project of MarinLink, a California non-profit corporation exempt from federal tax under section 501(c)(3) of the Internal Revenue Service #20-0879422.