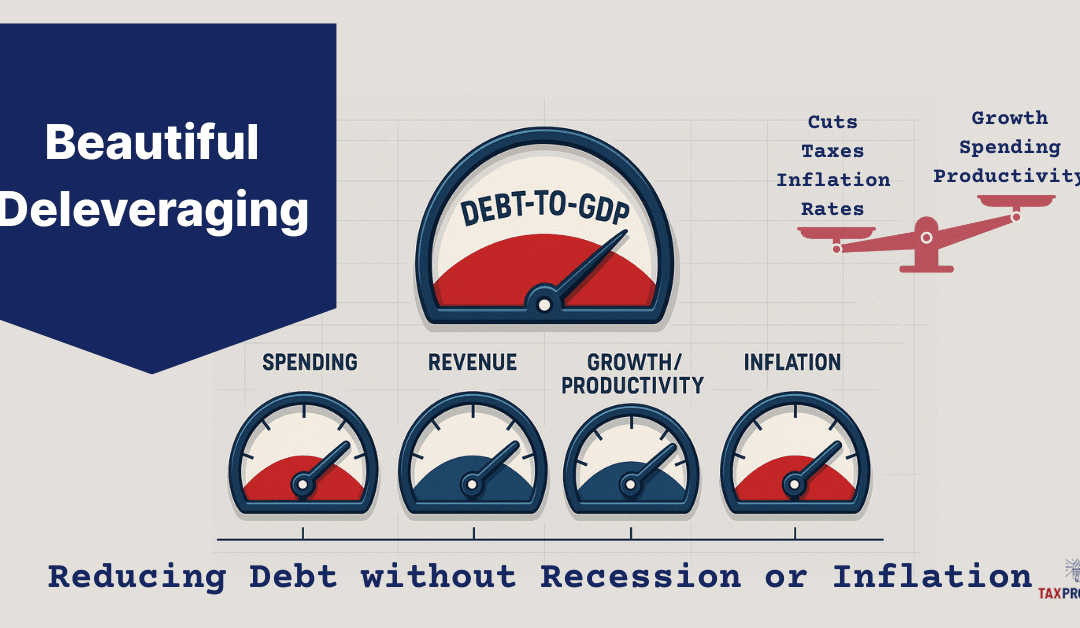

How the U.S. Could Reduce Debt Without Breaking the Economy

The U.S. National Debt just passed $38 trillion according to the US Treasury’s Debt to the Penny. [1][2] Not all debt is bad, but if it gets too large then debt can matter a lot, even those denominated in a fiat currency, because interest costs compound and grow they can crowd out other national priorities. Growing up your parents may have told you that it’s a lot easier to get into something, then to get out. That is especially true for debt, easy to get in, and painful to get out. Now that we have reached the point where interest payments are over $1 trillion annually, the US has crossed into that uncomfortable territory. The real challenge is to bring debt growth under control without causing a recession or a bout of high inflation. Ray Dalio, a billionaire hedge fund manager who has written books on Why Nations Succeed and Fail, and How Countries go Broke, popularized the idea of a “Beautiful Deleveraging” – a balanced, multi-year process that reduces the painful process of deleveraging when lowering debt burdens through a mix of growth, moderate inflation, controlled austerity, and targeted debt adjustments, rather than a painful deleveraging that could lead to recession, extreme reductions in services, tax increases, and austerity measures. [3][4]

This piece frames what a Beautiful Deleveraging could look like for the United States, why it’s hard, the challenges faced, and how policy could balance the Deflationary forces of tightening with the Inflationary tools sometimes used to ease the adjustment—aiming for a soft landing that improves the country’s long-run fiscal and economic health, while minimizing the pain along the way.

Current Status

National Debt: The National Debt stands at just over $38 trillion (gross) with over $30 trillion of which is Debt held by the public. [2]

Deficits: Structural Annual deficits running over $1trillion at around ~6% of GDP. [5][6]

Interest Costs: Net Interest over $1 trillion annually. The Congressional Budget Office (CBO) Long-Term Budget Outlook (March 2025), Net Interest reaches 5.4% of GDP by 2055, up from ~3.2% of GDP around 2025. [7][8] Independent analysis by the Committee for a Responsible Federal Budget (CRFB) highlights a related pressure point: by the 2050s, net interest would consume roughly 28% of federal revenues, absent policy changes. [9]

According to CBO’s latest long-term outlook, by 2055 total Federal outlays (spending) are projected at about 26.6% of GDP, with Net Interest (interest paid on National Debt) near 5.4% of GDP. That means that roughly one-fifth (~20%) of Federal spending will be used to pay interest on the debt. At that scale, interest costs rival or exceed most standalone programs and risk crowding out other priorities if unaddressed. [7][8][9]

What “Beautiful Deleveraging” Means

In Economic terms, Beauty is about reducing debt while avoiding (or at least minimizing) the painful parts of deleveraging and therefore managing that successfully can be Beautiful. Dalio’s Deleveraging framework was originally developed to explain past debt cycles and emphasizes a balanced mix of tools so that the economy can reduce debt without crashing demand and involves these components:

Spending Restraint (public and private demand constraint),

Income growth (real GDP growth),

Debt Restructuring or Terming out (Monetary intervention when necessary), and

A measured amount of Money/Credit creation (Moderating and managing inflation).

These components, when executed with great skill, political courage, and balance, can help the economy grow enough to ease debt ratios while avoiding a deflationary spiral. [3][4]

For a sovereign like the U.S., that balance translates into a policy with credible fiscal consolidation, productivity-oriented growth policies, and a monetary policy that avoids both runaway inflation and hard-landing deflation. Because the U.S. issues debt in its own currency with deep capital markets, it has more room to maneuver than most, but it is not immune to arithmetic: if interest rates (R) run above growth (G) (See our Article on R > G), debt ratios tend to rise unless deficits are reduced. CBO’s long-term projections foresee precisely this pressure in their future outlook. [9]

Pain Points: Why Deleveraging Is Hard

There is a reason it’s hard, in general large broad spending cuts, and more and higher taxes are not popular. While the components and levers are well known, it takes a healthy amount of political courage to propose policies that maybe unpopular, a great deal of skill and coordination to execute these policies, and likely a good amount of luck and good timing for a sustained period likely across several administrations. A deleveraging can proceed along two of these painful paths, spending cuts and tax increases, and each has tangible real-world consequences:

Spending cuts: Less public consumption and investment, fewer or slower growth in transfers, and potentially fewer (e.g. program eliminatinos) or lower service levels (e.g., processing times, enforcement, infrastructure maintenance). In macro terms, cuts are deflationary, they reduce aggregate demand, which can cool inflation but also growth and employment in the short run.

Tax increases: Higher effective tax rates reduce disposable income and/or after-tax returns to investment, is also deflationary. Design matters: broadening the base (fewer exemptions) generally distorts behavior less than steep marginal rate hikes, but either path tightens demand.

Because both mechanisms have a contractionary/deflationary impact and create conditions that can lead to recession, economic hardship, and job loss, a multi-year consolidation approach is part of Dalio’s framework. Instead of a fiscal cliff and extreme austerity based spending cuts; Dalio’s approach phases changes over time; and pairs tighter budgets with growth-friendly policies (innovation, expansion, permitting, skills, productivity increases) that lift the supply side. The goal is to keep nominal GDP growth (real growth + inflation) from collapsing, otherwise debt-to-GDP can rise even while you cut, because the revenue denominator shrinks.

Deleveraging Menu (and Their Trade-offs)

The Tax Project has outlined (See our Article: “Ways Out of Debt”) a non-exhaustive review of policy options to deleverage. Below we provide a summary group them by mechanism. [10]

1) Consolidation via Revenues (Tax Increases)

Summary: Revenue measures (Tax Increases) are deflationary near-term but can be structured to minimize growth drag (e.g., emphasize consumption/external taxes with offsets, or reduce narrow, low-value tax expenditures).

2) Consolidation via Outlays (Spending Cuts)

Summary: Spending cuts can be deflationary; pairing it with supply-side reforms (education/skills, streamlined permitting for productive investment, R&D incentives, labor force productivity growth) can mitigate growth losses and raise potential output over time.

3) Pro-Growth, Supply-Side Reforms (Growth)

Summary: Growth and Supply side reforms (e.g. Productivity, Innovation, Permitting, Energy inputs) that generate real productive growth is the least painful way to lower debt-to-GDP without relying on high inflation.

4) Inflation and Financial Repression (Print Money)

Summary: Modest inflation can ease real debt burdens, part of Dalio’s balance, while managing highly destructive excess inflation. That is why the “beautiful” approach uses only modest inflation alongside real growth, fiscal and monetary management, not inflation as the main lever. [7][9]

The Sooner we Start, the Easier it is

The bottom line is, the longer we wait the harder it gets, the problem will not go away on its own, it only gets worse over time. The 2025 CBO long-term outlook provides a forecast, and it doesn’t paint a great picture:

Debt Outlook: Debt held by the public rises toward 156% of GDP by 2055, under current-law assumptions. [8][11]

Outlays vs Revenues: Outlays (spending) climbs from ~23.7% of GDP (2024) to 26.6% (2055); revenues rise more slowly to 19.3% – expanding an already large and persistent structural gap. [8][12]

Net interest: Reaches 5.4% of GDP by 2055—roughly one-fifth of total federal outlays and around 28% of Federal revenues. [7][8][9]

Those numbers underscore the reason to start now: the later the adjustment, the harder the challenge required to stabilize debt. Conversely, a timely package that the public views as credible and fair can anchor long-term rates lower than otherwise, reducing the interest burden mechanically.

A “Beautiful” U.S. Deleveraging

The Tax Project does not propose or advocate specific policies, however a workable plan using the Dalio Framework would likely include a mix of the following components aimed to stabilize debt-to-GDP within a decade and then bend it downward while sustaining growth and guarding against excessive inflation relapse. A balanced approach:

A multi-year fiscal framework enacted up front allowing for a ordered and measured deleveraging.

Credible guardrails: Deficit targets linked to the cycle; a primary-balance path that improves gradually, with automatic triggers to correct slippage.

Composition: Roughly balanced between base-broadening revenues and spending growth moderation in the largest programs (phased in).

Quality: Protect high-return public investment; target lower-value spending and tax expenditures first.

Administration: Resource the revenue authority to improve compliance; align incentives and simplify.

A growth package to offset the deflationary impulse.

Supply-side reforms with high ROI: energy and infrastructure permitting; skilled immigration; workforce skills; competition policy that fosters innovation and productivity tools.

Private-sector: Reduce regulatory frictions that impede capex expenditures in goods and critical infrastructure.

Monetary-Fiscal Coordination in the background—not Fiscal Dominance.

Monetary-Fiscal Coordination: The Federal Reserve keeps inflation expectations anchored; it does not finance deficits but it can smooth the adjustment by responding to the real economy and anchoring medium-term inflation near target. Over time, a credible Fiscal policy promoting growth helps bring Rates (R) down toward Growth (G), easing the arithmetic. [7][9]

Contingency tools (use sparingly)

“Terming out” Treasury debt Lock in more fixed, long-term loans and rely a bit less on short-term IOUs. Why it helps: If rates rise, less of the debt has to be refinanced right away, so interest costs don’t spike as fast. If the term premium is reasonable and the Fed is in an accommodative stance, shorter term lower rate treasuries maybe attractive to reduce Net Interest expenses.

Targeted restructuring (not the federal debt—specific borrower groups) Adjust terms for groups where relief prevents bigger damage (e.g., income-based student loan payments, disaster-area mortgage deferrals). Why it helps: Stops small problems from snowballing into defaults and job losses while the government tightens its own budget.

This mix qualifies as “beautiful” by balanacing inflationary and deflationary elements. It shares the burden across levers; it avoids hard financial shocks; it relies primarily on real growth + structural balance rather than high inflation or sudden austerity. Done credibly, long-term rates fall relative to a laissez-faire (do nothing) approach, lowering interest costs directly and via lower risk premia. The country benefits both intermediate (by not inducing a recession and harsh economic measures), and long term freeing up revenue to more productive uses than Debt payments, and supporting growth.

Managing the Macro Balance: Deflation vs Inflation

All this sounds good, but the practical art is to offset deflationary consolidation with pro-growth supply measures, not with high inflation. Consider the balancing act between these different variables:

Consolidation (deflationary): Fiscal discipline reduces demand, manages structural gaps, good for taming inflation; risky for growth if overdone or badly timed.

Growth Reforms (disinflationary over time): Expand supply, lower structural inflation pressure; raise real GDP and productivity, improving the debt to GDP ratio.

Monetary Stance: Should keep inflation expectations managed; if growth softens too much, gradual monetary easing is available if inflation is on target.

Inflation temptation: Modest inflation can reduce some of the burden mechanically, but leaning on inflation as the adjustment tool can backfire if markets demand higher interest rate (term) premiums; nominal rates can rise more than inflation, worsening R > G and Net interest. CBO’s baseline already shows interest outlays rising markedly even without an inflationary strategy. [7][9]

A “Beautiful Deleveraging“ aims too creates a “soft landing” keeping nominal GDP growth positive, inflation expectations managed, and real growth strong enough that debt-to-GDP falls without creating undue Economic hardships. Managing each of these variables with the often blunt tools available, many of which don’t manifest for months, or years is quite the magic trick, requiring patience, skill, and acumen.

Risks and Pitfalls

The road ahead can be bumpy and full of challenges, managing the risks is key to a successful deleveraging. Here are some areas that can derail a “Beautiful Deleveraging.”

Front-loaded austerity that slams demand into a downturn or recession; a gradual path anchored by rules and automatic stabilizers is safer and creates less hardships. It means that we will endure less pain over a longer period. Some may want to rip the band aid off and take the measures all at once.

Policy whiplash (frequent reversals) that destroys credibility and raises risk premia (higher Interest rates); stable consistent policies beat one-off “grand bargains” and political vacillations.

Over-reliance on rosy outlooks; plans should make conservative growth assumptions, and reasonable baselines.

“Kicking the can” down the road with laissez-faire policies until interest dominates the budget, leaving painful, crisis-style adjustments as the only option is the biggest of all the Risks. CBO’s outlooks illustrates how waiting raises the eventual cost, and negative consequences. [7][8][9]

Is it Worth it?

On the surface, that’s an easy question, however the answer may pit generations against each other each with their own point of view and different perspectives. Current generations at or near retirement who may not see the worst effects of a laissez-faire policy may see the risk of recession, and cut backs in service as an unacceptable change to their Social Contract which they may have worked a lifetime under a set of expectations that they counted on. Younger generations, may see it as generational theft, placing an undue burden on them for debt they had little or no part in creating. Both are valid perspectives, however, the long term effects of a “Beautiful Deleveraging” will deliver these positive durable payoffs for the Country:

Out of Doom Loop: High debt is a trap, as out of control interest expenses rise, debt grows and the gap between revenue and debt rises in a self reinforcing doom loop. Breaking that loop is key to a healthy economy.

Lower Interest burden: As debt drops, so does Net Interest expenses. Instead of crowding out other expenses, revenue is freed up to other National Priorities (e.g. Healthcare, Education, Infrastructure, Social Services, Surplus, Sovereign Wealth). [7][9]

Greater Macro resilience: With manageable debt exogenic shocks, pandemics, wars, financial events, give the Government financial space to manage these events without taking on negative levels of debt.

Higher Trend growth: When consolidation is paired with genuine productivity reforms, lower debt ratios are correlated with higher growth, supporting living standards and the tax base. [14][15][16]

Summary

A “Beautiful Deleveraging” is but one way to approach the intractable problem of high debt. It represents a reasonable approach that balances near term realities with long term impacts. Our choices now will define the America of the future, and the quality of life younger Americans will have and future generations will inherit. Will it be painless? Probably not, it will likely require some sacrifice and discipline. The challenge wasn’t created in a short period, and it won’t be solved in a short period. Is it achievable? If we face the truth with candor about trade-offs, accept phased steps that the public deems fair, and have a bias toward investments that raise long-term productive capacity, than it is possible. The biggest question is the will of the American people. That, more than any single policy, will determine our future. At the Tax Project we will always bet on informed Citizens making the best choices for America – we will always bet on America. That defines the essence of a “Beautiful Deleveraging.” [3][4][10]

Citations

[1] U.S. Department of the Treasury, America’s Finance Guide: National Debt (accessed Oct. 2025): “The federal government currently has $37.98 trillion in federal debt.” (fiscaldata.treasury.gov)

[2] Joint Economic Committee (JEC) Debt Dashboard (as of Oct. 3, 2025): Gross debt ~$37.85T; public ~$30.28T; intragovernmental ~$7.57T. (jec.senate.gov)

[3] Ray Dalio, What Is a “Beautiful Deleveraging?” (video explainer). (youtube.com)

[4] Ray Dalio, short-form clip on “beautiful deleveraging.” (youtube.com)

[5] Reuters coverage of CBO near-term deficit path (FY2024-2025). (reuters.com)

[6] Associated Press summary of CBO’s 10-year outlook (debt +$23.9T over decade; drivers). (apnews.com)

[7] Congressional Budget Office, The Long-Term Budget Outlook: 2025 to 2055—headline results: net interest 5.4% of GDP by 2055; outlays path. (cbo.gov)

[8] Peter G. Peterson Foundation, summary of the 2025 Long-Term Outlook: outlays to 26.6% of GDP; interest path and historical context. (pgpf.org)

[9] Committee for a Responsible Federal Budget (CRFB), analysis of CBO 2025 outlook: interest consumes ~28% of revenues by 2055; R > G later in the horizon. (crfb.org)

[10] Tax Project Institute, Ways Out of Debt: US Options for National Debt (June 14, 2025). (taxproject.org)

[11] Reuters recap of CBO long-term debt ratio (public debt ~156% of GDP by 2055). (reuters.com)

[12] CBO, Budget and Economic Outlook: 2025 to 2035 (context for near-term path). (cbo.gov)

[15] Cecchetti, S. G., Mohanty, M. S., & Zampolli, F. (2011). The Real Effects of Debt (BIS Working Paper No. 352). Bank for International Settlements.

[16] Eberhardt, M., & Presbitero, A. F. (2015). Public debt and growth: Heterogeneity and non-linearity. Journal of International Economics, 97(1), 45-58.

The “Debasement Trade” is a prominent investment strategy in current finance, defined by the systematic movement of capital out of assets denominated by sovereign promises, such as fiat currencies and traditional fixed-income securities, and into assets characterized by verifiable, finite supply, often referred to as “hard assets” [1]. This strategy is fundamentally a defensive measure, designed to preserve the real value of wealth against the risk of the currency’s diminishing purchasing power, which results from accelerating national debt and large/rapid monetary expansion [2]. The shift reflects a growing, fundamental loss of confidence in the long-term fiscal solvency of major economies, especially the United States, whose currency serves as the global reserve.

I. Historical Context: Debasement as a Sovereign Tool

The act of currency debasement, the reduction of a currency’s intrinsic value without altering its face value, has been a recurring fiscal strategy throughout history. While the methods have evolved, the economic rationale remains consistent: to increase the effective money supply to meet government financial needs, typically to fund large expenditures or manage mounting debts [3].

Physical Debasement: The Precedent

In the ancient and medieval worlds, debasement was a physical process. The Roman Empire offers a classic example, where successive emperors reduced the silver content of the denarius over several centuries [4]. By substituting precious metals with cheaper base alloys, the government could mint a greater volume of currency from the same reserves, allowing the Treasury to stretch its resources for state expenses. This practice, however, led directly to rising prices (inflation) as merchants recognized the coin’s diminished intrinsic worth.

Another significant example occurred in 16th-century England under King Henry VIII, a period often cited as the “Great Debasement” [5]. To finance ongoing conflicts, the silver purity of English coinage was drastically reduced (From over 90% to as low as 25%). This act, while providing short-term funding for the Crown, destabilized domestic and international trade, leading to public mistrust and prompting the widespread hoarding of older, purer coins—an economic phenomenon later formalized as Gresham’s Law (“bad money drives out good”) [5].

The Structural Shift to Fiat Debasement

The transition to a fiat monetary system fundamentally redefined debasement. Following President Nixon’s 1971 decision to suspend the convertibility of the U.S. dollar into gold, the global financial system moved entirely away from the commodity-backed anchors of the Bretton Woods agreement [6] (See our Article on Bretton Woods). In this modern context, debasement is not about physical manipulation but about administrative action: the unconstrained expansion of the money supply through central bank policy. The erosion of a currency’s value is now primarily a function of excessive issuance relative to underlying economic productivity [7].

US M2 Money Supply

Figure 1 Source: Federal Reserve

II. The Conditions of the Modern Debasement Trade

The current period is characterized by macroeconomic conditions that have accelerated investor concern and institutionalized the Debasement Trade as a key portfolio consideration.

The Scale of Sovereign Indebtedness

The primary catalyst is the unprecedented scale of the U.S. National Debt, which is over $37 trillion [8]. Unlike previous debt cycles, the current trajectory is sustained by structural spending (23 consecutive years with deficit, last 5 $trillion+), regardless of the political party in power [9]. This fiscal reality presents governments with a limited set of options: implement politically unpalatable spending cuts or tax hikes, or employ the politically more palatable solution of allowing the currency’s value to decline.

The Debasement Trade is predicated on the rational assumption that policymakers will inevitably choose the latter, utilizing monetary tools to reduce the real burden of the debt and its service costs [1]. Through inflation, the real value of the debt owed to bondholders is effectively diminished over time, a process often described as “financial repression.”

Investor Flight to Scarcity

The response from institutional investors has been explicit. Citadel CEO Ken Griffin has been a vocal proponent of this thesis, characterizing the current market environment as a “debasement trade” [10]. Griffin notes a tangible shift in capital, with investors seeking to “de-dollarize” and “de-risk their portfolios vis-a-vis US sovereign risk” by accumulating non-fiat assets [10].

This trend is observable through market data:

Currency Depreciation: The U.S. dollar index (DXY) has experienced significant periods of sharp depreciation against major currencies and, more dramatically, against hard assets like gold [11].

Reserve Diversification: Globally, the dollar’s share as the primary reserve currency held by central banks has been steadily declining, reaching multi-decade lows [12]. This signals a structural move by foreign governments to reduce reliance on the U.S. dollar, further supporting the debasement thesis [13].

US Dollar Valuation

Figure 2 Source: Federal Reserve

III. Monetary Policy, QE, and Hyper-Liquidity

The mechanics of modern debasement are inextricably linked to central bank interventions, specifically Quantitative Easing (QE).

Quantitative Easing and Money Supply Growth

QE, a policy initiated following the 2008 Financial Crisis and dramatically expanded during the 2020 COVID pandemic response, involves the central bank (the Federal Reserve) creating new electronic money to purchase vast amounts of government and mortgage bonds [14]. This injects large amounts of money (hyper-liquidity) into the financial system, resulting in an exponential, historically unprecedented surge in the M2 money supply (See Figure 1) [14].

This expansion is the engine of modern debasement. When the volume of money in circulation grows at a pace far exceeding the underlying growth in the economy’s productive capacity, the result is an inevitable loss of the currency’s value [15].

Inflation as the Mechanism of Debasement

The consequence of this imbalance is widespread inflation, which acts as the functional manifestation of currency debasement. Inflation is not merely a rise in prices but a measurable loss of the currency’s ability to retain its value [15]. Some consider this type of inflation a hidden tax (See our Article on Is Inflation a Stealth Tax?). Data confirms this erosion: significant cumulative price increases over recent five-year periods have fundamentally lowered the purchasing power of the dollar [10].

The Debasement Trade views inflation as structural rather than temporary—a direct result of governments financing massive deficits through the printing press, effectively taxing the population through reduced purchasing power rather than legislative mandate.

US Inflation

Figure 3 Source: Federal Reserve

IV. Political Debate and the Precedent of the Plaza Accord

The current anxiety surrounding debasement is focused on specific policy discussions within Washington concerning the intentional manipulation of the dollar’s value.

The Deliberate Devaluation Thesis

Certain U.S. economic advisors, notably within the Trump administration, have argued that the dollar’s status as the world’s reserve currency creates a structural “overvaluation” that persistently harms U.S. trade competitiveness [16]. Proponents of this view suggest that managing a controlled depreciation of the dollar is a necessary measure to correct global trade imbalances and support domestic manufacturing [16].

This thesis has led to policy suggestions, sometimes grouped conceptually under the name “Mar-a-Lago Accord.” These suggestions include strategies such as utilizing tariffs to adjust global currency levels or even taxing foreign holders of U.S. Treasury debt [16]. Such discussions signal a willingness by policymakers to consider actions to achieve fiscal and trade goals, even at the expense of currency stability (Inflation).

Purpose: The Plaza Accord was a multilateral agreement signed by the G5 nations (France, West Germany, Japan, the United Kingdom, and the United States) [17]. Its specific goal was to engineer an orderly depreciation of the U.S. dollar against the Japanese yen and German Deutsche Mark. At the time, the U.S. dollar was considered significantly overvalued due to high U.S. interest rates and robust capital inflows, which led to a massive U.S. trade deficit [18].

Mechanism: The participating nations agreed to coordinate currency market interventions, specifically selling U.S. dollars, to achieve the desired depreciation [18].

Outcome and Relevance: The Accord successfully achieved its short-term goal, weakening the dollar significantly [18]. However, it ultimately failed to deliver long-lasting correction to the underlying U.S. trade imbalances because the structural domestic factors—namely, low private savings and high government borrowing—remained unaddressed [19].

The historical parallel is crucial: while a new “accord” might temporarily achieve a devaluation target, the Debasement Trade argument suggests that without fundamental fiscal discipline, any managed decline will merely lead to renewed instability and require further monetary interventions.

The Official Stance

Despite the policy discussions, U.S. Treasury Secretary Scott Bessent has publicly distinguished between short-term currency fluctuations and long-term policy [20]. He maintains that the core of the U.S. “strong dollar policy” is to take long-term steps to ensure the dollar remains the world’s reserve currency, focusing on U.S. economic growth and stability, rather than obsessing over the exchange rate [20]. This distinction is intended to reassure global markets that the U.S. is not actively pursuing the dollar’s demise, even if domestic fiscal and monetary choices suggest otherwise.

V. Implications for Citizens and the Move to Hard Assets

The consequences of currency debasement are most keenly felt by the average citizen, whose financial well being may depend on the dollar’s stability. This is especially true after the post COVID rapid inflation period felt by most Americans who are now keenly aware of the negative impacts of inflation.

Inflationary Wealth Transfer

Debasement operates as a stealthy wealth transfer mechanism [21].

Erosion of Fixed Income: Citizens holding dollar-denominated assets, such as savings accounts, fixed pensions, and bonds, see the real value of their wealth diminish steadily [7]. This is especially punitive for retirees and those on fixed incomes.

Asset Price Distortion: While nominal asset prices (stocks, real estate) reach record highs in dollar terms, this surge is often an illusion. When these assets are measured against hard assets like Gold or Bitcoin, the appreciation is significantly tempered, reflecting the currency’s dilution rather than pure economic growth [22].

This disparity: those who are asset-rich (owners of real estate, commodities, or equities) are protected, while the working class and cash holders are negatively effected as their wages and savings buy less in real terms.

The Embrace of Hard Assets

The Debasement Trade is the strategic answer to this inflationary trap. Investors are choosing assets defined by their scarcity:

Gold (Traditional Hedge): Gold has served as a reliable store of value and inflationary hedge for millennia, its value enduring precisely because it cannot be created by a central bank [23]. Surges in the gold prices directly reflect the decline in the dollar’s relative value [12].

Bitcoin (Digital Scarcity): Bitcoin has been increasingly adopted as a contemporary hard asset [1]. Its maximum supply of 21 million coins is secured by cryptography and network consensus, rendering it immune to sovereign fiscal or monetary manipulation [2]. Its inclusion in the Debasement Trade reflects a redefinition of “hard money,” moving beyond the physical limitations of precious metals to the mathematical certainty of code [22]. The dramatic appreciation of Bitcoin is viewed by many investors not as a speculative frenzy, but as a rational re-pricing of mathematical scarcity relative to infinitely expanding fiat currency [1].

USD vs Hard Assets

Figure 4 Source: TradeView

VI. Conclusion: A Structural Shift

The Debasement Trade is more than a momentary market tactic; it is a structural investment shift reflecting deep seated concerns over fiscal integrity of the world’s leading economies. Driven by high and persistent debt accumulation, coupled with the unconstrained power of central banks to expand the money supply through QE, the trade represents a fundamental shift in investor trust, from faith in government promises to reliance on the verifiable scarcity of hard assets. As long as the structural imbalance between monetary creation and productive capacity persists, the strategic movement toward assets like gold and Bitcoin will continue to be a defining feature of the global financial landscape.

Webull (syndicated from Bloomberg/Benzinga). (2025, July 3). U.S. Treasury Secretary Bessent refuted claims that the recent depreciation of the U.S. dollar would affect its status as the world’s major currency. https://www.webull.com/news/13098149616067584 (Webull)

Understanding the Role of Bond Vigilantes and Government Fiscal Management

Bond markets play a pivotal role in any economy, serving as the mechanism by which governments raise money to fund their operations and programs. However, these markets are not just passive—they react to the fiscal and monetary policies of a government. If those policies are perceived to be risky and irresponsible, bond investors can invest elsewhere lowering demand for bonds and driving up interest rates and making it more expensive for governments to borrow money. This phenomenon is referred to as the actions of bond vigilantes. But before we delve into the role of bond vigilantes, it’s essential to understand the broader economic framework within which they operate—particularly the concepts of monetary policy, government debt, and how these influence the broader bond market.

Monetary Policy: What It Is and Why It Exists

Monetary policy refers to the actions taken by a country’s central bank (in the U.S., the Federal Reserve) to manage the supply of money, control inflation, stabilize the currency, and achieve sustainable economic growth. The main goal of monetary policy is to regulate inflation while also promoting economic stability. By adjusting the money supply and interest rates, the central bank can influence economic activity, employment levels, and consumer spending.

The Tools of Monetary Policy

The Federal Reserve has a few core tools that it uses to implement Monetary Policy:

Open Market Operations (OMOs): This is the most commonly used tool. OMOs involve the buying and selling of government securities, such as Treasury bonds, in the open market. By buying bonds, the Fed increases the money supply, effectively lowering interest rates. Conversely, by selling bonds, it reduces the money supply and raises interest rates. This helps control inflation and smooth out economic cycles.

Discount Rate: This is the interest rate at which the central bank lends to commercial banks. If the Fed lowers the discount rate, borrowing becomes cheaper for banks, and they, in turn, can lower interest rates for consumers and businesses. This helps to stimulate economic activity. When credit is looser this is often referred to as an Accommodating policy. If the Fed raises the discount rate, it makes borrowing more expensive, which can slow down an overheating economy. When credit is tighter this is often referred to as a Restrictive policy.

Reserve Requirements: This is the portion of depositors’ balances that commercial banks must hold as reserves and not lend out. By adjusting reserve requirements, the Fed can influence the amount of money that banks can lend to consumers and businesses. A lower reserve requirement increases the amount of money in circulation, while a higher reserve requirement decreases the amount of money available for lending.

The main goal of these tools is to ensure that the economy doesn’t experience too much Inflation (which can erode purchasing power) or Deflation (which can lead to reduced economic activity and a slowdown in growth).

Why Does Monetary Policy Exist?

Monetary policy exists to stabilize the economy and control inflation. Without a central authority to regulate money supply and interest rates, economies can fall into cycles of boom and bust—hyperinflation, recessions, and depressions. By setting the right monetary policy, the Fed helps to smooth these fluctuations, keeping the economy on a stable growth path and avoiding extreme imbalances.

Inflation Control: High inflation can reduce the value of currency and savings. It distorts pricing and makes long-term planning more difficult for businesses and consumers. The Fed uses monetary policy to control inflation within a target range (often around 2%).

Economic Stability: By adjusting interest rates and influencing credit availability, monetary policy helps to prevent excessive inflation or deflation. It also moderates the effects of recessions by stimulating demand when needed.

In the US the Federal Reserve is the Central Bank for the country, and is said to have a dual mandate that aligns with these goals. 1) Price Stability – the current Fed has set a target of 2% inflation to manage the Inflation Control. 2) Maximum Employment – to insure economic activity leads to Economic stability and job growth.

The Government and Debt: Why Borrowing is Necessary

A government typically borrows money by issuing bonds, which are essentially debt securities. These bonds are bought by investors (including domestic and foreign institutions, banks, and individuals) who receive regular interest payments (the coupon) in exchange for lending money to the government. Governments borrow for several reasons:

Funding Deficits: Governments often run deficits—when their expenditures exceed revenues (mainly from taxes). Borrowing allows them to cover the difference.

Public Investment: Borrowing allows governments to fund long-term investments in infrastructure, education, and healthcare without immediately raising taxes.

Crisis Management: In times of crisis (such as wars, natural disasters, or economic downturns), governments often need to borrow heavily to provide relief and stabilize the economy.

How Government Debt and Fiscal Policy Relate to Bonds

The government uses bonds as a way to raise the necessary capital (money) to finance its operations. Treasury bonds are seen as a safe investment, particularly for large institutions and foreign governments, because they are backed by the full faith and credit of the U.S. government. However, how much debt the government takes on and the policies it implements around borrowing can have a profound impact on the bond market.

When the government issues debt in the form of Treasury bonds, it promises to pay the principal back at a later date, along with interest at the agreed-upon rate. The interest rate (or yield) on these bonds is determined by market conditions, inflation expectations, and the government’s perceived ability to meet its financial obligations.

As long as investors trust that the government will honor its debt obligations, Treasuries remain attractive, even in times of economic uncertainty. However, if market participants lose confidence in the government’s ability to manage debt responsibly, and perceive higher risks, they may sell their holdings in Treasury bonds, driving interest rates (yields) higher and making it more expensive for the government to borrow. This is where bond vigilantes come into play.

Bond Vigilantes: The Market’s Check on Government Fiscal Policy

The term bond vigilantes often carries a certain connotation of malevolence, as if these market participants are actively trying to harm the government by making its borrowing more expensive. However, this perception is a misunderstanding of the true nature of bond vigilantes. In reality, bond vigilantes are not malevolent actors but rational participants in the marketplace who are simply reacting to perceived additional risks in a bond offering. These market players are primarily concerned with the quality of the asset—in this case, government debt—and the risks associated with it.

A member of a volunteer committee organized to suppress and punish crime summarily (as when the processes of law are viewed as inadequate)

broadly: a self-appointed doer of justice

The bond vigilantes’ role is a market-driven check on fiscal policy. They do not act out of malice, but rather as a response to the increased risk they perceive in holding government bonds as an investment. When the government takes actions that might increase inflation, debt, or the likelihood of default thereby increasing risk, bond vigilantes react by demanding higher returns (higher yields) to compensate for that added risk. If they do not feel they are being adequately compensated for those risks, they will look elsewhere to deploy their capital, such as in alternative investments like stocks, foreign bonds, or commodities.

Rational Market Mechanism of Bond Vigilantes

At their core, bond vigilantes are rational actors in a market where the value of assets (in this case, U.S. Treasuries) is determined by supply and demand. When the risks associated with these assets increase, the price of bonds decreases, and in turn, yields increase. This is a natural market response to the perceived decline in the quality of an asset.

The underlying logic is straightforward:

If investors believe that a government’s fiscal policies could lead to higher inflation, growing debt, or the risk of default, they will demand higher yields to compensate for that perceived risk.

If the government does not adjust its policies in response to this feedback, bond prices will fall further, yields will rise, and the cost of government borrowing will increase, reflecting the higher risk.

In essence, bond vigilantes are not acting with a specific agenda to punish the government, but are simply making a rational decision based on the changing risk profile of the asset they are holding. They are demanding higher returns because they believe the risk of holding government debt has risen, whether due to concerns about fiscal mismanagement, inflation, or geopolitical instability.

Bond Vigilantes and the Price of Treasury Bonds

A simple way to understand how bond vigilantes work is to look at the relationship between bond prices and yields. When a government’s fiscal policies are perceived as risky, investors may begin selling off existing bonds. As the supply of bonds increases in the market, their prices fall, and because bond prices and yields are inversely related, the yields rise. If an investor is facing increased risk, they will demand higher yields to compensate for that risk.

Consider this scenario: if the U.S. government were to increase its debt or adopt inflationary policies that the market views as unsustainable, bond vigilantes would begin selling off Treasuries, driving prices down and pushing yields higher. This would increase the cost of borrowing for the U.S. government, making it more expensive to finance operations. This serves as a natural check on fiscal policy, encouraging governments to adopt more sustainable spending and borrowing practices to avoid the consequences of escalating borrowing costs.

Who are the Bond Vigilantes?

Bond vigilantes are just Bondmarket participants who react to changes in government fiscal and monetary policies, not some special group policing Government. These large investors demand higher returns (higher yields) to compensate for perceived risks in holding government debt, especially when policies lead to rising debt, inflation, or fiscal instability.

Key Players and Their Rough Participation Levels

Institutional Investors (40%): This includes mutual funds, pension funds, and insurance companies. They are significant holders of government bonds and act as bond vigilantes when fiscal policies raise concerns about inflation or debt sustainability.

Hedge Funds (30%): These funds are more speculative and nimble, using leverage to bet on macroeconomic shifts. Hedge funds play a large role in short-term bond market movements and often lead the charge in demanding higher yields when fiscal mismanagement is perceived.

Foreign Governments and Sovereign Wealth Funds (20%): Countries like China, Japan hold large amounts of U.S. debt. If they feel U.S. debt is becoming too risky, they can quickly influence bond yields by selling Treasuries.

Individual Investors (10%): Although less influential, retail investors who own savings bonds or retirement accounts can react to inflation or concerns about government debt by shifting away from U.S. Treasuries.

Bond Vigilantes Summary

Bond vigilantes are not and organized group of malevolent actors seeking to damage the government, but rational players responding to perceived risks in an investment. Their actions are simply part of a larger market dynamic where risk is constantly assessed, and investors make decisions based on the expected return on their investments. When investors sense that the risk of holding government bonds is higher, they will demand higher compensation, in the form of higher yields, or else they will move their capital elsewhere. This is a healthy mechanism that ensures governments stay accountable to the markets, forcing them to manage debt and fiscal policy more prudently.

In summary, bond vigilantes play a crucial role in keeping governments in check. They are rational actors responding to increased risk by adjusting the yield on government bonds. Their actions force governments to reconsider their fiscal policies or face higher borrowing costs, which could in turn lead to a reassessment of the sustainability of their debt and spending practices.

The Role of Bond Vigilantes in History: The 1970s and 1980s

The 1970s and 1980s are often cited as the classic example of bond vigilantes in action. During this period, the U.S. experienced high levels of inflation (peaking at 13.5% in 1980) and growing government debt, which caused bond investors to demand higher yields.

1. The 1970s: Rising Debt and Inflation

The 1970s were marked by stagflation—a combination of high inflation and stagnant economic growth. The U.S. was dealing with the aftermath of the Vietnam War, rising oil prices, and growing government spending on entitlement programs.

The Federal Reserve, under Arthur Burns, was criticized for keeping interest rates too low for too long, allowing inflation to spiral. Bond vigilantes responded by selling Treasuries, pushing yields higher.

Bond yields soared, and the U.S. government found itself in a difficult position: borrowing costs were rising, and the value of the dollar was being eroded by inflation.

2. The 1980s: Volcker’s Response

In response to the bond vigilantes’ actions and the growing economic instability, Paul Volcker, Chairman of the Federal Reserve, implemented a tight monetary policy, raising interest rates to historic levels (peaking at 20% in 1981) to combat inflation.

This move successfully curbed inflation, but it came with significant economic pain: the U.S. entered a recession, and unemployment soared. However, the aggressive action by Volcker was necessary to restore credibility in the bond market and get inflation under control.

The 1980s marked the beginning of a new era where bond vigilantes played a critical role in holding governments accountable for fiscal and monetary policy.

The Parallels to Today

The current economic environment bears similarities to the 1970s and 1980s, with rising debt levels, inflation concerns, and fiscal challenges. Bond vigilantes may re-emerge if investors perceive that the U.S. government is not effectively managing its fiscal policies. Several factors contribute to this emerging concern:

Rising Debt: The U.S. national debt now exceeds $36 trillion, and the government’s annual debt servicing costs are rising. Last year alone the interest payments on the National Debt were over $1 Trillion, surpassing the Military budget. This is drawing comparisons to the 1980s, when rising debt levels led to higher borrowing costs and market instability.

Inflation: After years of low inflation, recent inflationary pressures have re-emerged, driven by factors such as supply chain disruptions, rising energy prices, and large government spending. The Fed has recently calmed this is down by raising interest rates, but if inflation continues to rise, bond vigilantes may demand higher yields as compensation for inflation risk.

In recent months, U.S. Treasury bonds have experienced notable volatility, challenging their long-standing reputation as the world’s safest investment. This shift has been driven by a combination of factors, including escalating national debt, inflationary pressures, and political uncertainties.

The yield on the 10-year Treasury note has risen significantly, reflecting increased investor concerns. For instance, in April 2025, the yield surged to 4.5%, its highest level in over a decade. This uptick was attributed to factors such as rising inflation expectations and a growing national debt [2].

Ongoing Fiscal policy, including maintaining Tax Cuts and Jobs Act (TCJA) tax cuts, increased government spending, and fiscal deficits further strain bond market tension. The CBO projects National Debt to continue to expand, raising questions about the sustainability of U.S. fiscal policy [3,5].

Investor sentiment has been further impacted by credit rating agencies downgrading the U.S. credit rating. In May 2025, Moody’s downgraded the U.S. credit rating to Aa1 from Aaa, citing concerns over increasing government debt [4].

The Consequences of Rising Yields: A Fragile Economic Environment

The US is in a somewhat fragile situation with the highest National Debt since World War II. This could limit the Federal Reserves options if U.S. bond yields were to rise dramatically, especially in response to concerns over fiscal policy, the consequences would be severe:

Higher Borrowing Costs: The government would face increased debt servicing costs, consuming a significant portion of the federal budget.

Inflation: Higher yields could signal more inflation, eroding the value of the dollar and reducing purchasing power.

Dollar Devaluation: If the market loses confidence in U.S. fiscal management, the value of the U.S. dollar could fall, and the U.S. could lose its status as the world’s reserve currency.

Global Financial Turmoil: A loss of confidence in U.S. Treasuries could lead to a flight to other assets like gold or the Chinese yuan, destabilizing the global financial system.

Dire Impact of 15% Interest Rates

If the U.S. were to face 15% interest rates, similar to the 70’s era Volcker policies, the annual interest payments on the national debt would surge to around $5.4 trillion—exceeding the entire $4.9 Trillion in Federal revenue of the U.S. for 2024 [1]. This would create an untenable fiscal situation:

All federal revenues would be consumed by interest payments, severely limiting the ability of the government to fund other essential services, such as social programs, defense, and education.

The U.S. would likely face a massive budgetary crisis, tax increases and cuts to critical programs would become unavoidable.

Rising borrowing costs could push the U.S. into default or require debt restructuring, both of which would have catastrophic effects on global financial markets.

Conclusion

Bond vigilantes serve as an important market discipline mechanism that can force governments to reconsider fiscal and monetary policies. When investors perceive that a government is mishandling its debt or failing to control inflation, they respond by selling bonds, driving yields higher. This forces the government to either adjust its policies or face higher borrowing costs. The lessons from the 1970s and 1980s show us that fiscal mismanagement and rising debt can lead to economic pain, especially if bond vigilantes push back.

In today’s world, with rising debt levels and inflation concerns, the potential for bond vigilantes to re-emerge is high. If the U.S. government fails to manage its fiscal policies effectively, it could face the consequences of higher interest rates, a devalued dollar, and a loss of confidence in U.S. Treasuries—leading to economic instability both domestically and globally. The fragility of the current environment makes it important for the government to manage this fragile state with sustainable fiscal policies and prudent monetary policies before bond vigilantes act for them and force their hand into dire consequences for the US.

Mary Meeker’s highly anticipated “USA, Inc.” report, released in March 2025 by Bond Capital, once again delivered a meticulously researched financial assessment of the United States. Following her seminal 2011 “USA Inc.” report, this 2025 iteration provides a critical updated snapshot, viewing the U.S. federal government through the lens of a corporate balance sheet and income statement. The core message remains consistent: America’s fiscal trajectory is a pressing concern, though the urgency and prescribed solutions vary wildly depending on one’s economic philosophy.

The original 2011 “USA Inc.” report served as a stark wake-up call, highlighting accelerating debt accumulation and growing unfunded liabilities, particularly in Social Security and Medicare [1]. It laid out a business-like accounting of the nation’s finances, suggesting that without significant changes, the U.S. was heading towards an unsustainable path.

Themes and Key Findings from USA, Inc. 2025

Fast forward to March 2025, and the latest “USA, Inc.” report paints a picture of deepening fiscal challenges. The delta from 2011 is not merely a quantitative increase in debt; it’s a qualitative shift where previously projected liabilities have materialized and accelerated, exacerbated by recent global events and policy responses.

Key findings and themes from the USA Inc. 2025 report:

Escalating National Debt: The national debt has surged to levels exceeding historical peaks relative to GDP, projected to continue its upward trajectory [2]. Figure 3

Crowding Out by Interest Payments: A significant and alarming finding is the rapid growth in net interest payments on the debt, which are now consuming an ever-larger portion of the federal budget, crowding out other critical federal investments like infrastructure, education, or defense [3]. Figure 4

Accelerated Unfunded Liabilities: The “epic” and rising nature of off-balance sheet liabilities, primarily for entitlements like Social Security and Medicare, continues to be a central theme. These commitments amount to multiples of the on-book debt, a warning bell that was already ringing in 2011 but is now blaring louder [1, 4]. Figure 2

Deteriorating Net Worth: Mirroring a corporate entity, the report likely shows a continued deterioration of USA Inc.’s net worth, implying a diminished financial flexibility to handle future national crises or unexpected economic shocks [1]. Figure 1

Figure 1 Deteriorating Net Worth, USA Inc.Figure 3 Escalating National Debt, USA Inc.

Figure 2 Unfunded Liabilities, USA Inc.Figure 4 Crowding out by interest payments, USA Inc.

Economic Interpretations: A Spectrum of Views

This grim outlook, however, isn’t universally accepted. Mainstream economics broadly encompasses traditional (neoclassical) views and Keynesian economics. Traditional economists often emphasize the importance of balanced budgets, fiscal discipline, and minimal government intervention, fearing that large deficits lead to crowding out of private investment and inflationary pressures. Keynesian economics, while acknowledging the long-term need for fiscal sustainability, emphasizes the role of government spending in stimulating demand during economic downturns, arguing that deficits can be beneficial when the economy is operating below its potential.

Modern Monetary Theory (MMT) represents a more heterodox, almost “post-Keynesian,” perspective. MMT posits that a sovereign government, which issues its own fiat currency, cannot technically “run out of money” and therefore isn’t constrained by debt in the same way a household or business is [6]. From an MMT perspective, the numbers presented in “USA, Inc.” might be seen not as an impending crisis, but rather as an accounting of necessary public spending to achieve societal goals, with inflation being the true constraint, not debt levels. Proponents of MMT would likely argue that government spending creates the very financial assets that fund the debt, and that fears of “crowding out” are overblown for a currency issuer [6].

Support for MMT remains a minority view [10] within the broader economics community. While it has gained increased public discussion, particularly since the 2008 financial crisis and in response to discussions around large-scale public spending, most mainstream economists, including many Keynesians, remain skeptical of its core tenets regarding government debt limits. They typically acknowledge a currency-issuing government’s ability to print money but emphasize the severe inflationary and currency devaluation risks associated with doing so without corresponding real economic output [7].

Conversely, mainstream economists and fiscal conservatives, supported by research from institutions like the Congressional Budget Office (CBO) [2], Brookings Institution [3], and the Peter G. Peterson Foundation [4], see the escalating debt as a significant long-term threat. These analyses consistently project that without policy changes, deficits will remain unsustainably high, leading to increased interest costs that consume a growing share of the federal budget.

The Impact If Nothing Is Done

If the trends highlighted in “USA, Inc. 2025” remain unaddressed, the potential economic ramifications could be severe and far-reaching:

Increased Taxes and/or Reduced Public Services: To service the growing debt, the government would eventually face difficult choices: raise taxes, cut spending on essential public services (like education, infrastructure, or defense), or a combination of both [5, 9].

Crowding Out of Private Investment: As the government borrows more, it competes with the private sector for available capital. This can drive up interest rates for businesses and consumers, making it more expensive for companies to invest and expand, ultimately stifling innovation and economic growth [5].

Stagflation Risk: An uncontrolled increase in the money supply to finance deficits, coupled with supply-side constraints, could lead to stagflation—a damaging combination of stagnant economic growth, high unemployment, and rising inflation [8].

Devaluation of the Dollar: Sustained large deficits and a perceived inability to manage debt could erode international confidence in the U.S. dollar. This could lead to a devaluation of the currency, making imports more expensive, reducing purchasing power for Americans, and potentially undermining the dollar’s status as the world’s reserve currency [9].

Reduced Fiscal Flexibility: A high debt burden leaves the government with less capacity to respond to future crises (e.g., pandemics, natural disasters, economic recessions) without further destabilizing its finances [2, 5].

The Importance of Government Financial Literacy

The underlying message of “USA, Inc.” – both the 2011 and 2025 versions – transcends partisan economics: government financial literacy is paramount. For citizens to make informed decisions and hold their elected officials accountable, a basic understanding of the nation’s financial statements is crucial. Meeker’s report, while crafted with an investor’s precision, is seemingly intended for a broad audience, distilling complex financial data into digestible charts and narratives.

Paradoxically, while the report aims for public comprehension, its detailed nature means it will likely be consumed and debated most rigorously by researchers, academics, economists, and financial industry professionals. Yet, those who will be most profoundly impacted by the underlying fiscal events – average citizens whose future taxes, public services, and economic opportunities are at stake – may be the least likely to fully engage with or understand the nuances of the document. This highlights a critical challenge: translating complex fiscal realities into actionable insights for the very public it seeks to inform. While there maybe disagreement over the impact, the trends and path are troubling and we hope that all Americans make informed choices regarding America’s future.

[7] Mankiw, N. G. (2020). A Skeptic’s Guide to Modern Monetary Theory. NBER Working Paper No. 26650. National Bureau of Economic Research. https://www.nber.org/papers/w26650

Tax Project Institute is a fiscally sponsored project of MarinLink, a California non-profit corporation exempt from federal tax under section 501(c)(3) of the Internal Revenue Service #20-0879422.