Why USASpending, Treasury, OMB, CBO can be factual and still not match

If you have ever tried to look up how much the Federal Government “spent” and found one number on USAspending, another in a Treasury report, and another in a document from the Office of Management and Budget (OMB) or the Congressional Budget Office (CBO), you are not imagining things. The numbers rarely if ever match exactly. That is confusing for a simple reason: people may assume all Federal spending numbers are trying to answer the same question. They are not.

Each maybe accounting for different reporting of money. Some sources are showing money the government was legally allowed to use. Some are showing money the government committed to spend. Some are showing money that actually left the government’s accounts. Some are showing projections, or estimates rather than final recorded totals. And some are designed for public transparency at the contract and grant level, while others are designed to serve as the government’s official accounting summary. For example Treasury’s Combined Statement is the official publication of Federal receipts and outlays, while USASpending is the government’s public spending transparency site built from multiple reporting systems and data feeds.[1][2]

That is why a person can find several different federal “spending” numbers that are all real, all official, and still not directly comparable. The problem is usually not that one source is lying. The problem is that each source is built for a different purpose. However, for example, calling something USASpending and then having to explain it is NOT the actual spending of the Federal government, but the obligations and some outlays, can understandably come across as misleading, and maybe even outright false to some.

This article explains the basic terms, the main organizations, where the data come from, why the numbers differ, and where readers should go depending on what they are actually trying to find. For readers who want the larger context of how the federal budget is proposed, enacted, apportioned, and executed, see Tax Project’s Budget Process Explainer.[9]

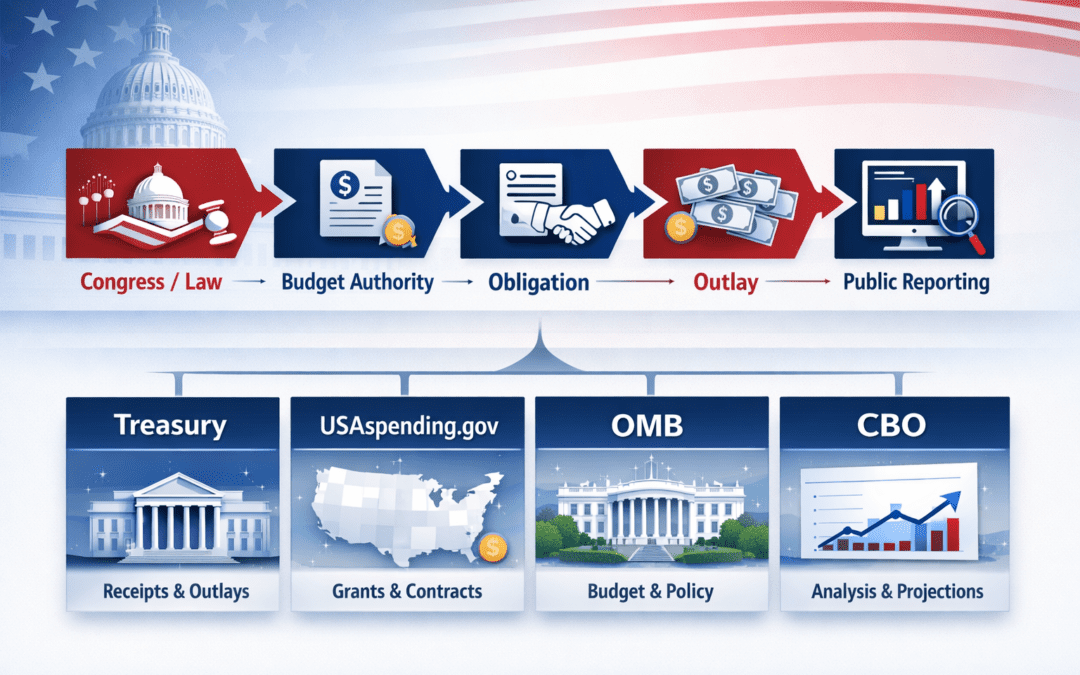

Key Terms

Before comparing websites and agencies, it helps to define the basic terms.

Budget authority is the legal permission to commit (spend) Federal funds (money). Congress provides this authority through appropriations or other laws.[3]

Obligations are legal commitments to spend, not the actual spend. If an agency signs a contract, awards a grant, commits to salaries, or incurs another binding commitment, that creates an obligation.[3][4]

Outlays are money actually paid out, or Spent. These are the checks, cash disbursements, electronic transfers, or other payments used to satisfy those obligations.[3]

These terms are related, but they are not the same thing. The Congressional Budget Office explains obligations as legally binding commitments and outlays as the disbursement of funds to settle those commitments.[3] USASpending explains the same distinction in simpler public-facing language: an obligation is a promise to spend, while an outlay is the actual spending.[4]

That difference sounds technical, but it matters a great deal. Much of the public confusion around federal spending comes from people comparing one source that tracks obligations with another source that tracks outlays, or from comparing a projection with an actual payment total.

Simple Example

Suppose you take out a $50,000 bank loan to remodel your kitchen.

Budget Authority (Permission): The bank approves you for up to $50,000. That is similar to budget authority. You are allowed to use that amount, but the money has not all been spent yet.

Obligation (Commitment): You then sign a contract with a builder for $42,000. That is similar to an obligation. You have made a legal commitment, but the builder has not been fully paid yet.

Outlay (Spend): The builder asks for $10,000 upfront, $15,000 halfway through the project, and the remaining $17,000 at completion. Those payments are similar to outlays. Cash leaves your account over time as the work is performed.

In this example, your authority to spend is $50,000, your legal commitment is $42,000, and your actual spending happens in installments. If someone looked only at your signed contract, they might say you “spent” $42,000 but that was only the obligaton. If they looked only at your first payment, they might say you spent $10,000. Both would be describing something real, but they would be describing different stages and accounting of the process.

Federal spending works much the same way. Congress provides legal authority. Agencies obligate money through contracts, grants, salaries, or benefits. Then outlays occur when money is actually disbursed.[3][5]

Budget Process

This article does not provide a full budget-process guide, but a little background helps.

At a high level, Congress enacts funding and legal authority. The Office of Management and Budget (OMB) apportions most executive branch budgetary resources and oversees budget execution. Agencies then obligate funds and later record or make outlays as payments occur. The Treasury department collects and publishes governmentwide financial information, and agency data also flow into public transparency tools such as USAspending.[5][6]

This larger chain matters because each major Federal source sits at a different point, and intentionally tracks a different set of data. Some are focused on legal authority and execution controls. Some are focused on cash reporting. Some are focused on analysis for Congress. Some are focused on public-facing transparency.

Readers who want the broader walk-through of this process can see the Tax Project’s article on the Federal Budget process here: The Federal Budget Process Explained.

Federal Government Organizations

A large part of the confusion comes from people seeing acronyms without understanding the role of each Governmental organization.

The U.S. Department of the Treasury(Treasury) is the Federal government’s main authorative source for spending and cash outlays. Treasury publishes the Monthly Treasury Statement, which summarizes monthly receipts, outlays, deficit or surplus, and financing on a modified cash basis, and it publishes the Combined Statement, which Treasury describes as the official publication of receipts and outlays of the U.S. government.[1]

The Office of Management and Budget (OMB) is part of the Executive Office of the President. OMB helps prepare the President’s Budget, oversees budget execution across the executive branch, apportions budgetary resources, and defines many of the concepts and classifications used in Federal budgeting. OMB also publishes historical budget tables and guidance such as Circular A-11 that is often referenced as Spending by various sources.[5][6][7]

The Congressional Budget Office (CBO) is Congress’s nonpartisan budget analysis office. It does not serve as the government’s master accounting ledger. Instead, it provides Congress with cost estimates for legislation, budget and economic outlooks, baseline projections, and plain-language explanations of budget concepts. These numbers may be used in media when discussing spending and budgets. [3][8]

USASpending.gov is the federal government’s public spending transparency site. It is designed to let users explore contracts, grants, loans, recipients, agencies, vendor awards, locations, and federal accounts. It is useful for tracing where money was obligated and, in many cases, where outlays were reported, but it is not the same thing as Treasury’s official annual governmentwide receipts-and-outlays statement.[2][4] In other words, in contrast to the sites naming, it is mostly Obligations, and some Outlays, but not truly “Spending” on an accounting outlay basis.

Each of these sources is official. Each is useful. But each is built to answer a different type of question.

Public Confusion

Because there are so many accounting contexts for spending, the public often hears a phrase like “the government spent $X” without context as to what that number refers to. It could be:

money Congress made available (Budget Authority),

money an agency legally committed (Obligation),

money actually paid (Outlay),

an estimated future amount (Estimate),

or a rounded analytical figure in a budget document.

Since many citizens may not understand the differences, that missing context is where the confusion starts.

If one person quotes Treasury, another quotes USAspending, another quotes OMB, and another quotes CBO, they may all be citing real Federal numbers. But they may be pulling numbers from different reporting systems, different points in time, and different definitions of spending. That can make the disagreement sound larger than it really is or distort the numbers. Unfortunately, it maybe our own public officials who use these numbers to distort topics to their advantage by making a misleading claim sound more precise than it is.

Where to find information

The practical question most readers care about is not which acronym is most important. It is where they should go for the answer they want.

Where to Find Information

If you want to know…

Best place to start

Why

How much the federal government actually paid out overall (Spending)

Treasury is the government’s official receipts-and-outlays anchor. Use the Monthly Treasury Statement for current monthly and year-to-date totals, and the Combined Statement for the annual official publication.

How much an agency obligated, which Contracts or Grants it issued, who received the money, or where it went (Obligations, some Outlays)

Good for readers who need the full process, not just the reporting differences.

Table 1

That table is the simplest answer to most reader questions. People often use the wrong source not because the source is bad, but because they are asking it to do something it was not built to do.

Why the Numbers Differ

To help unravel the confusion, there are four main reasons federal spending numbers differ across sources.

1. They are measuring different things

Treasury is mainly focused on receipts, outlays, and deficit totals. USASpending shows obligations and award-level detail. OMB presents budget concepts, classifications, and executive-branch historical tables. The Congressional Budget Office often provides rounded analytical figures, baselines, estimates, and projections.[1][3][5][8]

If you compare one source built around obligations to another built around outlays, there will be differences.

2. They sit at different stages of the spending pipeline

Obligations usually occur before outlays. A department can obligate funds for a contract or grant in one fiscal year and outlay the money over several years. That is common in procurement, construction, and many grant programs. Other programs, such as entitlement payments, may outlay more steadily and quickly.[3][5]

3. They use different reporting systems and scopes

USASpending is not fed from a single, perfectly unified source. It draws from multiple reporting systems and combines account-level and award-level data. Its documentation also notes that not all government entities report under the same requirements, including the legislative and judicial branches.[2]

Treasury’s role is different. It is producing the government’s official governmentwide receipts-and-outlays publications, not an award explorer.[1]

4. Reporting quality and timing vary

USAspending notes that more recent years generally have better-quality data, that agency financial-system data begin later than some award data, and that award-level outlay reporting before fiscal year 2022 may be incomplete. It also notes a delay in some Department of Defense and Army Corps of Engineers contract data.[2][4] Our own experience has shown us that values on their website can change years after the fact (which is why we stopped caching some of the data).

That means a reader looking for a neat, single, perfectly comparable “Federal spending number” across every system may end up disappointed. The systems overlap, but they do not function the same way.

FY 2025 as a real example

Fiscal year 2025 is a good example because official year-end figures are available.

Treasury’s Combined Statement for FY 2025 reported approximately $5.235 trillion in receipts, $7.010 trillion in outlays, and a $1.775 trillion deficit.[1]

Office of Management and Budget’s FY 2027 Analytical Perspectives materials, reported FY 2025 unified receipts of approximately $5.236 trillion, unified outlays of approximately $7.011 trillion, and a unified deficit of $1.775 trillion.[5][7]

Congressional Budget Office’s FY 2025 is described in more rounded analytical terms, referring to roughly $5.2 trillion in revenues, $7.0 trillion in outlays, and a deficit of about $1.8 trillion.[8]

Those numbers are close, but not identical. That small difference is exactly the kind of thing readers notice and wonder about. OMB itself explains that although its figures are generally consistent with Treasury’s, differences can arise because of later reporting corrections, classification changes, and conceptual differences between OMB and Treasury reporting.[7] CBO’s presentation is less suited to one-for-one matching because its role is analytical, not to serve as the government’s final accounting statement.[8]

USASpending is different again showing $10.3 trillion in obligations, trillions of dollars different than outlays. It is extremely useful for exploring obligations, awards, recipients, agencies, and accounts, but it is not best thought of as the government’s single final annual top-line cash scoreboard for “spending.” It is a transparency platform, not the same type of publication as Treasury’s Combined Statement.[2][4]

Figure 1 Source: USASpending

USASpending: What it is good for, and what it is not

What it’s good for:

USASpending is often the best place to start when the reader wants to know:

which agency made an award,

which company or recipient got the money,

what federal account funded it,

where the work was performed,

or how much was obligated on a contract or grant.

That is a major strength, mostly our governments obligations. It give a great sense of how much our country is committed to now and into the future, and where (who) that money is obligated to.

What it’s not for:

However, if the question is: “What is the official total amount the federal government spent for the year?”, the US Treasury is the better starting point.[1][2] Oddly, and as we have expressed confusingly, USASpending is NOT the best source to look for what is “spent” by the Federal Government, that accounting is best shown by the outlays in the MTS report from the Treasury.

This distinction matters because public debates often blur the difference between a transparency portal and an official governmentwide accounting publication. They are related, but they are not interchangeable and as we show above, the differences can be in the trillions of dollars, not just a rounding error. Citizens armed with these “facts” maybe wielding information incorrectly when used in different contexts.

For readers who want a more feature-rich way to explore USAspending-based federal spending data, Tax Project’s Government Explorer is intended to provide a more navigable and feature rich front end while still drawing on USASpending data.

Why this matters

Informed citizens are the basis of our Republic, and the foundation of our Democracy. Our founding fathers understood that the protection of our country would rest on the knowledge and participation of it’s citizens, not just relying upon our elected officials. Public debate over Federal spending dictates many important parts of how our government is run, and what is prioritized and funded impacting the lives of all Americans. Politicians may use these terms interchangeably in contexts that often present their case in a favorable light. While some may call this dishonest, others may call it a lie, the common point is that if you don’t understand these terms you maybe manipulated by category or term confusion. While we believe that not all politicians are dishonest, it is up to citizens to understand the context, and be able to ascertain the accurate and factual information in the correct context on their own. When people quote different numbers from different systems without explaining what those numbers actually measure, understanding the terms, context, and sources will help you make more informed choices.

When one person cites obligations, another cites outlays, another cites a budget estimate, another cites a rounded CBO analytical total, and another cites Treasury’s official receipts-and-outlays statement. All may be using real figures. But real figures can still mislead when they answer different questions than what the reader thinks they do.

The better approach is to ask a more precise question first:

Am I trying to measure legal authority? (Budget Authority – Permission)

legal commitment? (Obligation – Commitment)

actual payment? (Outlays – Spend)

a budget estimate? (Estimate – Projection)

or a recipient-level spending record? (Award, Grantee)

Once that question is clear, the source usually becomes much easier to choose. Treasury is the best starting point for official overall outlay totals. USASpending is best for award and account exploration of obligations. OMB is best for executive-branch budget concepts and the President’s budget. The Congressional Budget Office is best for Congress’s independent estimates, projections, and cost analyses.

So is it simple, not unfortunately it is not. This does not remove all complexity, but hopefully it makes Federal spending data easier to understand. We encourage you to continue on your journey of Government Financial Literacy. Smarter Citizens, Stronger Country

The Anti-Deficiency Act (ADA) is Congress’s principal enforcement mechanism for its constitutional “power of the purse.” It bars federal officials from obligating or expending funds in excess of, or in advance of, appropriations; prohibits acceptance of voluntary services (with narrow emergency exceptions); prohibits obligations in excess of Office of Management and Budget (OMB) apportionments; and requires agencies to report violations to the President and Congress. In modern shutdowns, these prohibitions are the legal force that halts non-excepted activities unless and until Congress enacts appropriations or a continuing resolution. See 31 U.S.C. § 1341 (limitations on expending/obligating), § 1342 (voluntary services), and § 1517 (apportionment violations) [1–3, 5–6].

The same framework also empowers the executive branch—principally through OMB—to direct operational shutdown steps and to meter spending during the year through apportionments and reserves under 31 U.S.C. § 1512 and § 1513, subject to the Impoundment Control Act (ICA) and Government Accountability Office (GAO) oversight [4–6, 16].

Constitutional and Legal Foundations

Article I, § 9, cl. 7 of the Constitution provides: “No money shall be drawn from the Treasury, but in Consequence of Appropriations made by Law.” Congress operationalized that rule through the Anti-Deficiency Act, now largely codified through:

31 U.S.C. § 1341 (no obligations/expenditures above or before appropriations) [1].

31 U.S.C. § 1342 (no voluntary services except in narrow emergencies) [2].

31 U.S.C. §§ 1349–1351 (administrative sanctions and reporting to the President and Congress) [5].

31 U.S.C. §§ 1511–1519 (apportionment controls; violations of apportionment limits are ADA violations) [3–4].

The Government Accountability Office (GAO) calls the ADA one of the primary enforcement mechanisms of the appropriations framework, and its Principles of Federal Appropriations Law (“Red Book”) treats it as the backbone of budget execution discipline [6].

History: How and Why the ADA came about

1860s – 1880s: Origins, the problem of “Coercive Deficiencies”

After the Civil War and through the late 19th century, agencies (notably in the War and Navy Departments) developed the habit of entering obligations without available appropriations and then pressuring Congress to provide supplemental funds after the fact—so-called “coercive deficiencies.” Congress responded first with an 1870 appropriations rider (Act of July 12, 1870, ch. 251, § 7, 16 Stat. 251), later reenacted as Revised Statutes § 3679—the antecedent to today’s ADA [10]. Congress strengthened the regime in 1884 and again in 1905–1906 by adding the apportionment discipline and penalties, so agencies could not front-load obligations and then create deficiencies (1905: 33 Stat. 1257; 1906 added criminal penalties) [9–10].

Sponsors and partisanship: The 19th-century Anti-Deficiency restrictions were riders to large appropriations bills carried by floor managers rather than single named sponsors. The emphasis was institutional control, not partisan signature [9–10]. Riders are provisions to larger bills, often used as policy bargains hitched to bills to insure passage of legislation (often appropriations).

1930s–1950: toward a modern control system

As executive budgeting centralized (Bureau of the Budget (BOB), predecessor to OMB), Congress overhauled execution rules in the General Appropriation Act of 1951 (enacted 1950). Those changes formalized apportionment authority and prohibited obligations in excess of apportionments—now codified at 31 U.S.C. § 1517—and allowed limited reserves to realize savings [3, 10]. Legislative histories note Rep. William F. Norrell (D-AR) as a House sponsor/manager of key 1950 execution amendments—an indicator of bipartisan, process-oriented reform rather than a partisan initiative [11].

1982: positive-law codification (bipartisan and executive-signed)

In 1982 Congress enacted Title 31 as positive law (Pub. L. 97-258) to “revise, codify, and enact without substantive change” existing fiscal statutes—including the ADA—into the structure we use today. The bill H.R. 6128 was sponsored by Rep. Peter W. Rodino, Jr. (D-NJ), cleared both chambers by voice/unanimous consent, and was signed by President Ronald Reagan (Sept. 13, 1982) [12].

1990: narrowing the “emergency” exception (OBRA-90)

Responding to disputes over the scope of “emergencies,” Congress amended 31 U.S.C. § 1342 in the Omnibus Budget Reconciliation Act of 1990 (OBRA-90) to state that “emergencies involving the safety of human life or the protection of property” do not include “ongoing, regular functions of government” whose suspension would not imminently threaten those interests. OBRA-90 was sponsored by Rep. Leon Panetta (D-CA) and signed by President George H. W. Bush (Nov. 5, 1990) [2, 13].

Summary: Modern legal framework

What the ADA prohibits and requires

No obligations/expenditures above or before appropriations. Officials may not “make or authorize an expenditure or obligation exceeding an amount available” or “involve the Government in a contract… before an appropriation is made,” unless otherwise authorized by law. 31 U.S.C. § 1341 [1].

No voluntary services. Agencies may not accept voluntary services or employ personal services beyond those authorized by law, except for bona fide emergencies involving safety of human life or protection of property, as narrowly defined in the 1990 amendment. 31 U.S.C. § 1342 [2, 13].

No obligations against apportionments. Even with an appropriation, agencies cannot obligate/spend above OMB apportionments or allocations; violating an apportionment is itself an ADA violation. 31 U.S.C. § 1517 [3–4].

Mandatory reporting. Agency heads must report ADA violations to the President and Congress, with a copy to GAO, detailing facts and corrective actions. 31 U.S.C. § 1351; GAO publishes compilations and guidance [5–6].

Sanctions. Administrative discipline (including suspension/removal) applies for violations; knowing and willful violations of key provisions carry criminal penalties under 31 U.S.C. § 1350. Criminal prosecutions are rare; agencies usually impose administrative remedies and procedural fixes [5–6, 18–20].

GAO’s Red Book underscores that the ADA, combined with purpose/time/amount restrictions, is how Congress ensures the executive uses funds only as appropriated [6].

How the ADA governs Shutdowns and empowers Government Branches

The Shutdown logic

When an appropriation lapses, 31 U.S.C. § 1341 bars incurring obligations for affected activities; § 1342 bars acceptance of voluntary services; and § 1517 bars obligations in excess of apportionments. The only work that can lawfully continue is (i) authorized by law (e.g., multi-year/no-year funds, user-fee accounts, mandatory programs), (ii) falls within the narrow emergency exception of § 1342, or (iii) is necessary for an orderly shutdown [1–4, 14].

The Department of Justice Office of Legal Counsel (OLC) articulated the modern framework in the Civiletti opinions (1981) and a 1995 OLC memo refining the emergency and “necessary implication” doctrines; both are the basis for today’s practice [8–9, 14]. OMB Circular A-11, Section 124 operationalizes shutdowns: agencies must keep current lapse/contingency plans, and, once a lapse occurs, OMB directs initiation of orderly shutdown activities. Office of Personnel Management (OPM) furlough guidance aligns with A-11: non-excepted employees are placed on shutdown furlough; “excepted” personnel perform only those duties necessary to protect life/property or to support legally funded programs; and employees may not volunteer to work prohibited duties [6–7, 15].

Bottom line: the ADA is the legal brake that halts most operations during a lapse; OMB and OPM provide the playbook for how to stop [1–4, 6–7, 9].

Legislative branch (Congress) Power during shutdown

1) Hard stop without appropriations. The House and Senate control whether operations continue by enacting appropriations or a continuing resolution. The ADA makes non-excepted obligations unlawful absent that legislative action. 31 U.S.C. § 1341 [1, 6, 8–9].

2) Control through conditions and time limits. Congress can embed caps and conditions; exceeding those limitations can itself be an ADA violation, per OLC (e.g., “not to exceed” caps). This gives Congress fine-grained policy control via riders [5, 36].

3) Oversight leverage via mandatory reporting. ADA reporting to the President, Congress, and GAO gives committees a direct oversight tool. 31 U.S.C. § 1351; GAO ADA portal [5–6].

Executive branch (President & OMB) Power during shutdown

1) Direction of shutdown execution (procedural control). Under OMB Circular A-11, Section 124, OMB tells agencies when to initiate orderly shutdown steps, what must be in contingency plans, and how to classify activities as exempt (legally funded) or excepted (narrow emergency/necessary implication). Agencies act through those plans; OMB coordinates. This is a real (though bounded) form of executive operational power during a lapse [6–7].

2) Apportionment power – year-round metering of obligations. Outside a lapse, OMB uses apportionments to meter how much of an appropriation is available to obligate (by quarter, project, or activity) to avoid deficiencies and ensure economical execution. That authority is grounded in 31 U.S.C. § 1512 and § 1513. If an agency obligates above an apportionment (or agency subdivision limits under § 1514 regulations), it violates § 1517, an ADA breach reportable to Congress and the President [3–4].

3) “Necessary implication” and defining excepted functions (during lapses). OLC’s 1981/1995 opinions recognize that some functions must continue when other statutes would be defeated without supporting work (e.g., to protect life/property, maintain constitutional functions, or support ongoing legally funded activities). OMB/agency plans translate those legal standards into concrete “excepted” workforces. This is a gatekeeping role – OMB and agencies decide what qualifies, but their discretion is cabined by the narrow 1990 definition in § 1342 and OLC’s tests [2, 8–9].

4) Limits: the Impoundment Control Act (ICA) and GAO review. OMB’s apportionment and reserve tools cannot be used to effectuate policy deferrals or impoundments that Congress has not authorized. GAO concluded OMB violated the ICA when it withheld Ukraine security assistance by footnoting apportionments to make funds temporarily unavailable for obligation; OMB disputed GAO’s view, but the decision remains a prominent constraint on using apportionments to pursue policy ends [16].

5) Live leverage examples. Shutdown-era guidance—such as how OMB and agencies describe eligibility for work vs furlough, or the expectation of back pay under the Government Employee Fair Treatment Act of 2019—can shape the negotiating environment even while remaining bounded by statute. The key takeaway is that procedural control (sequencing, classifications, pacing) gives the Executive Branch influence, while substantive authority (whether money exists) remains Congress’s [6–7, 14–16].

Net: The ADA constrains the executive from operating beyond legal funding, but within that constraint OMB exercises material procedural and timing control—both during lapses (sequencing shutdown and defining excepted functions) and during execution (apportionments). Congress retains the decisive substantive control: whether, when, and on what conditions funds exist at all [1–6, 8–9, 16].

Enforcement, Reporting, and Consequences

Enforcement: Agencies manage (often via the agency’s Office of Inspector General, OIG) whether an Anti-Deficiency Act (ADA) violation occurred, impose administrative discipline, and file the mandatory report to the President and Congress under 31 U.S.C. § 1351. The OMB polices execution through apportionments and Circular A-11; exceeding an apportionment is itself an ADA violation that the agency must report. The GAO provides independent legal decisions, audits, and publishes ADA violation compliance reports, but does not enforce

Reporting: Agencies must report ADA violations to the President and Congress, with a copy to GAO, including facts, causes, and corrective actions. GAO maintains public resources and compilations. 31 U.S.C. § 1351; GAO ADA resources [5–6, 32–34].

Consequences: Administrative discipline (suspension/removal) is typical for negligent management errors; 31 U.S.C. § 1350 provides criminal penalties for knowing, willful violations. (Judge Advocate General [JAG] practice notes describe administrative discipline under a strict-liability standard for the underlying breach, with mens rea (must show specific intent) required only for criminal cases.) [5, 18–20] For criminal cases (rare), the Department of Justice (DOJ) – typically through U.S. Attorneys – prosecutes knowing and willful violations referred by an agency/OIG (sometimes flagged by GAO or OMB). Congress receives § 1351 reports, conducts hearings and oversight, and can tighten or condition future appropriations reinforcing accountability across the system.

Controversies and recurring Gray areas

The ADA is not without controversy, when a shutdown occurs, interpretations of the statutes create gray areas that each party and branch may try to exploit.

Scope of “necessary implication” and “authorized by law.” OLC recognizes some functions must continue when other statutes would be defeated without supporting work. Critics argue agencies occasionally read these exceptions too broadly; Congress narrowed § 1342 in 1990 to tether “emergency” to imminent threats [2, 9, 13].

What counts as “protection of property/life.” The line between routine operations and true emergencies is fact-bound. Agencies must document why a function is excepted in their A-11 plans; OMB reviews [6–7, 9].

Internal caps and conditions as ADA triggers. Department of Justice OLC has advised that exceeding internal caps or conditions embedded in an appropriation can itself constitute an ADA violation—giving Congress fine-grained policy control via riders [36].

Shutdown employment practices and back pay. The Government Employee Fair Treatment Act of 2019 (GEFTA) requires post-lapse compensation; how agencies and OMB frame the mechanics can affect expectations and pressure, but cannot override statute [14–15].

Apportionment overreach vs. execution discipline.31 U.S.C. § 1512 requires apportionment to prevent deficiencies and ensure economy; § 1517 makes exceeding apportionments an ADA violation. Used correctly, it’s neutral budget discipline; used to delay or condition funds for policy, it risks ICA violations [3–4, 16].

Practical takeaways (for practitioners and watchdogs)

During a lapse, assume “stop” unless funded or excepted. The default is to halt affected work; exceptions exist but are narrow, documented in agency plans, and coordinated with OMB. 31 U.S.C. §§ 1341, 1342; OMB A-11 § 124 [1–2, 6–7].

Multi-year/no-year funds are a lifeline—but still subject to apportionment. Activities with unexpired prior-year or permanent appropriations can continue if legally available and within apportionments. 31 U.S.C. §§ 1512–1513 [3–4].

Don’t accept “free help.” Voluntary services generally violate § 1342 unless an explicit, lawful authority applies; otherwise you can create an implied claim for pay [2, 35].

Exceeding an apportionment is an ADA violation, even if the appropriation has funds left. That is § 1517 in action [3–4].

Congress’s leverage is structural; OMB’s leverage is procedural. Congress decides whether and on what terms funds exist; OMB controls sequencing and the pace of execution within those terms (subject to ICA limits) [1–6, 16].

Conclusion

The Anti-Deficiency Act provides the operational legal framework for Congress control over Federal spending, the so called “Power of the Purse”. Born to end Coercive Deficiencies and strengthened with apportionments and reporting, it ensures that Federal officials/agencies cannot obligate or expend funds without legislative authorization. In governs Government shutdown activities: non-excepted activities must stop. It provides Congress leverage and control via appropriations/funding. At the same time, the ADA’s architecture (as implemented by OMB through A-11 and by agencies via contingency plans) gives the Executive branch real procedural power to direct how a shutdown is managed and how funds are metered during the year—bounded by statute, OLC opinions, and the Impoundment Control Act, and monitored by GAO [1–6, 8–9, 16]. For more, see our article on the Federal Budget Process.

Citations

[1] 31 U.S.C. § 1341 (limitations on expending/obligating amounts), Legal Information Institute. [2] 31 U.S.C. § 1342 (limitation on voluntary services; 1990 amendment narrowing emergencies), Legal Information Institute. [3] 31 U.S.C. § 1517 (prohibited obligations and expenditures in excess of apportionments), Legal Information Institute. [4] 31 U.S.C. § 1512 (apportionment and reserves) and § 1513 (officials controlling apportionments), Legal Information Institute. [5] 31 U.S.C. §§ 1349–1351 (administrative discipline; criminal penalties; reporting), govinfo/LII. [6] GAO, Principles of Federal Appropriations Law (“Red Book”) and ADA overview pages (role of ADA as primary enforcement). [7] OMB Circular A-11 (current), Section 124—Agency Operations in the Absence of Appropriations (shutdown procedures and OMB direction). [8] OLC (1981) “Civiletti” Opinion—Authority for the continuation of government functions during a lapse in appropriations. [9] OLC (1995) Memorandum—Government Operations in the Event of a Lapse in Appropriations (refining “necessary implication” and emergency tests). [10] Historical summaries of 1870/1884/1905–06 Anti-Deficiency provisions and their aims (ending “coercive deficiencies”). [11] Legislative notes indicating Rep. William F. Norrell (D-AR) as a sponsor/manager of the 1950 execution amendments. [12] Pub. L. 97-258 (Sept. 13, 1982): Positive-law codification of Title 31; H.R. 6128 sponsored by Rep. Peter W. Rodino, Jr. (D-NJ); signed by President Reagan. [13] OBRA-90 change to 31 U.S.C. § 1342—narrowing “emergency”; H.R. 5835 sponsored by Rep. Leon Panetta (D-CA); signed by President George H. W. Bush. [14] OMB/agency shutdown contingency plans and OPM furlough guidance aligning with ADA and A-11. [15] Government Employee Fair Treatment Act of 2019 (back-pay baseline after lapses). [16] GAO decisions on apportionment/ICA (e.g., Ukraine assistance), constraining OMB’s use of apportionments for policy ends. [18] 31 U.S.C. § 1349 (administrative discipline). [19] 31 U.S.C. § 1350 (criminal penalties). [20] Agency ADA violation compilations and GAO reporting instructions (annual ADA reports). [32–36] Additional GAO decisions and DOJ OLC advisories on voluntary services, internal caps, and shutdown boundaries (for deeper case-by-case applications).

The Federal government isn’t just a tax collector — it’s the largest redistribution engine in the country for funding to the States.

Each year, trillions of dollars in Federal taxes are collected from across all 50 states. That money is then redistributed through spending on public programs, infrastructure, grants, contracts, aid, and more. Much of that funding is redistributed back to the States.

But who gives the most — and who gets the most back? Is what you give, what you get back?

Today, we’re excited to launch our latest Tax Project Citizen tool, our Fund Flow app — a powerful, interactive tool that makes it easy to explore the financial relationship between each State and the Federal government.

What is Fund Flow?

Fund Flow is a data-driven web app that brings clarity to a complex topic. Using visually rich, interactive charts and maps, you can explore:

Which states are net contributors (giving more than they get)

Which states are net recipients (getting more than they give)

Whether you’re zooming in on your own State or comparing nationwide trends, Fund Flow gives you a clear view of where the money flows.

Why It Matters

This isn’t just about dollars and cents — it’s about understanding how our system works.

Most people don’t realize how much their state sends to Washington D.C. — or how much it gets back. Fund Flow gives everyone the tools to:

Understand where your tax dollars go

Stay informed about how Federal funding is redistributed

See which states benefit the most or least from Federal spending

Engage with real data in a clear, accessible way

Informed citizens are essential to a healthy democracy. By making these financial flows visible, Fund Flow helps you ask better questions, have smarter conversations, and hold decision-makers accountable.

Explore Fund Flow

Try out Fund Flow today! It’s free to use and built for everyone — from citizens and educators to journalists, researchers, and policymakers.

As the US Federal Fiscal year draws to a close each September, a peculiar phenomenon grips government agencies across the United States. Known colloquially as “The Big Flush,” this annual event sees a dramatic surge in government spending as departments rush to exhaust their remaining budgets. This practice, driven by the “use it or lose it” mentality, raises important questions about fiscal responsibility, government efficiency, and the delicate balance of power between the legislative and executive branches.

The Appropriations Process and Legal Framework

To understand the year-end spending surge, we must first examine the federal budget process. The U.S. Constitution grants Congress the “power of the purse,” giving it ultimate authority over government spending. This power is exercised through the annual appropriations process, where Congress determines funding levels for various federal agencies and programs.

The Congressional Budget and Impoundment Control Act of 1974 (ICA) further refined this process, establishing procedures for congressional budgeting and placing limits on the executive branch’s ability to withhold appropriated funds. This legislation was a direct response to President Nixon’s attempts to impound funds allocated by Congress, a practice the Supreme Court later deemed unconstitutional in Train v. City of New York (1975)[2].

Under the ICA, the President is required to spend all appropriated funds unless specific procedures are followed to request rescissions (i.e Cancel spending) or deferrals (i.e. Delay spending). For rescissions, the President must propose them to Congress, which then has 45 days to pass a rescission bill. If Congress fails to act within this timeframe, the President must release the funds as originally appropriated[5]. Deferrals, which temporarily delay spending, can be overturned by either house of Congress passing a resolution of disapproval[1].

The “Use It or Lose It” Phenomenon

The legal requirement to spend appropriated funds, combined with the annual budget cycle, has given rise to the “use it or lose it” mentality among government agencies. This phenomenon refers to the tendency of departments to rapidly spend their remaining budget allocations in the final weeks of the fiscal year, fearing that unspent funds will be returned to the Treasury and potentially lead to budget cuts in subsequent years[1].

Research has empirically demonstrated the existence of this year-end spending surge. A study by economists Jeffrey Liebman and Neale Mahoney, cited in the National Bureau of Economic Research (NBER) working paper, found that federal agencies spend an average of 4.9 times more in the last week of the fiscal year than in a typical week[1]. This dramatic increase in spending raises concerns about the quality and necessity of last-minute spending.

Implications for Taxpayer Money and Government Efficiency

The year-end spending surge has significant implications for the efficient use of taxpayer money. Critics argue that this practice encourages wasteful spending on low-priority or unnecessary items simply to meet (exhaust) budgets. The rushed nature of these purchases may lead to poor decision-making, inadequate vetting of contracts, and reduced value for money.

Liebman and Mahoney’s research supports these concerns, suggesting that the quality of spending decreases during the year-end surge. They found that many of these last-minute expenditures fall below the social cost of funds, effectively meeting the definition of wasteful spending[1].

The social cost of funds is an important concept in evaluating government spending. It refers to the total cost to society of using public resources for a particular purpose, including both direct costs and indirect costs such as economic distortions caused by taxation[13]. When year-end expenditures fall below this threshold, it means that the societal benefits derived from the spending are less than the overall cost to society of providing those funds[1].

Moreover, this pattern of spending can distort the overall allocation of resources within the government. Agencies may prioritize easily executable, short-term expenditures over more strategic, long-term investments that could yield greater public benefit but require more time to plan and implement.

The Executive Branch Conundrum

While the ICA and subsequent court decisions have reinforced Congress’s power of the purse, this strict approach to budget execution creates a conundrum for the executive branch. On one hand, the President and federal agencies are legally obligated to spend appropriated funds as directed by Congress. On the other hand, this requirement may hamper the executive branch’s ability to respond flexibly to changing circumstances or to implement more efficient spending strategies.

The executive branch, with its day-to-day management of government operations, may be better positioned to identify areas where spending could be reduced or reallocated more effectively. However, the current system provides limited flexibility to do so without going through the cumbersome rescission or deferral processes outlined in the ICA. The bottom line is rarely do planning estimates (Congress Appropriations) match the real world actual expenses.

This tension between compliance and efficiency creates a challenging environment for agency leaders. They must balance their legal obligation to spend appropriated funds with their responsibility to use taxpayer money wisely. The fear of budget cuts in future years if funds are left unspent further complicates this balancing act, potentially incentivizing suboptimal spending decisions in order to protect budget.

Congressional and Judicial Support for the Power of the Purse

Despite these challenges, both Congress and the courts have consistently upheld the legislative branch’s primacy in budgetary matters. The Supreme Court’s decision in Train v. City of New York (1975) effectively removed the presidential power of impoundment, reinforcing Congress’s control over spending[2].

This stance is rooted in the constitutional separation of powers and the principle that the power to appropriate funds is a fundamental check on executive authority. If the executive branch could unilaterally decide not to spend appropriated funds, it would effectively nullify Congress’s constitutional power to levy taxes and borrow money[9].

However, this strict interpretation of the power of the purse creates a paradox. While it aims to prevent executive overreach and ensure that the will of Congress (and by extension, the people) is carried out, it may inadvertently promote inefficiency and waste in government spending.

Mechanism for Improvements

While the Tax Project does not make policy recommendations, it is clear that Process improvements and new mechanisms could improve overall results. Potential improvements could include a more flexible system with ongoing budget feedback loops, allowing for more dynamic allocation of resources throughout the fiscal year. Additionally, a mechanism by which the executive and Congress could work together more closely on budget execution could be beneficial. This could involve tying budget flexibility to legislative outcomesachieved by the executive team, rather than focusing solely on the amount spent[9].

Furthermore, consideration could be given to mechanisms that support longer-term projects. The current annual budget cycle can make it challenging to plan and execute multi-year initiatives effectively. A system that allows for better management of funds across fiscal years for approved long-term projects could lead to more strategic investments and reduce the pressure for year-end spending[9].

Conclusion

The “big flush” of year-end government spending highlights the complex interplay between fiscal responsibility, government efficiency, and constitutional principles in the United States. While the current system, rooted in the Congressional Budget and Impoundment Control Act, aims to uphold Congress’s power of the purse and prevent executive overreach, it also creates incentives for potentially wasteful spending practices.

Addressing this issue requires a delicate balance. Any reforms must respect the constitutional separation of powers and Congress’s fundamental role in determining government spending. At the same time, they should aim to promote more efficient and effective use of taxpayer money throughout the fiscal year.

As the debate continues, it is clear that finding this balance is crucial for ensuring good governance and fiscal responsibility in the modern era. The challenge lies in developing a system that maintains strong legislative control over spending while providing the flexibility needed for efficient and responsive government operations. Only through careful consideration and bipartisan cooperation can meaningful reforms be achieved to address the “big flush” phenomenon and improve the overall management of federal resources.

Have you ever paused to consider how well you truly understand the financial workings of our government? While most of us take steps toward personal financial literacy—learning how to budget, save, and invest—do we give the same attention to how our tax dollars are being managed? If you’re like most Americans, the answer is likely no even though most Americans spend a quarter or their working life contributing to it. It’s time to change that.

Government Financial Literacy (GFL) isn’t just about understanding numbers; it’s about equipping yourself with the knowledge to assess how effectively our government generates, spends, and manages public funds. Unfortunately, the Politicians, we often entrust, may be the ones misleading us or outright lying to the public distorting the truth. Sure, some people delegate their personal finances to professionals, trusting experts to manage their money. But even they check in, review their financial statements, and have a system of accountability. Shouldn’t we do the same with our government? How else can we expect citizens to make informed decisions at the voting booth or participate in policy debates to see if they are aligned with their values?

Why Should You Care About GFL?

If you’ve ever wondered, “Why should I care?”—consider this: You wouldn’t hand over your personal finances without keeping an eye on where your money is going, would you? Even if you hire a financial advisor, you maintain oversight, ask questions, and review the outcomes. But when it comes to government spending, many citizens blindly trust that things are being managed correctly, with no mechanism for accountability or understanding.

This mindset can have serious consequences. Understanding government finances is more than knowing how much we pay in taxes. It means comprehending the direct, secondary, and long-term effects of public policies. Tax decisions don’t just affect this year’s budget—they shape our lives, economic future, determining the quality of infrastructure, education, healthcare, and national defense.

Let’s face it: the numbers can be overwhelming. Public debt in the trillions? Spending bills in the billions? It’s easy to get lost, but those figures have real consequences, this isn’t Monopoly money. What are the long-term effects of growing debt? How does inflation affect public services? Without GFL, you may feel left in the dark on critical issues that impact your life, your community, and future generations.

The Stakes Are High

We live in an increasingly complex world, where the financial decisions of our government play a critical role in shaping not only our present but also our future. As the size, scope, and services of Governments continue to increase it becomes even more important now than ever. With rising public debt, inflation, global competition, and economic inequality, GFL should not be considered optional— it’s critical to our democracy. We need to understand how resources are allocated, which programs are funded, and how those decisions impact both our immediate needs and long-term stability for our families and country.

The stakes of public finance are much higher than we realize. Take public debt: it’s not just an abstract figure or a problem for future generations; it affects taxes, interest rates, and public services today. Without proper understanding of how government financial policies work, we’re left vulnerable to misinformation, unable to assess the sustainability of policies being proposed.

It’s Your Civic Duty

Make no mistake, GFL is not just for policy wonks or economists. Every American has a duty to understand the financial health of our government. Participating in our democracy requires more than just voting; it requires understanding the policies we’re voting on and the long-term impacts they will have.

When you have GFL, you’re not just informed about today’s numbers—you can project the ripple effects of policy decisions. You understand that cutting taxes today might mean fewer public services tomorrow. You grasp the long-term consequences of deficit spending, and you’re empowered to ask the tough questions: Where is this money going? How will it be repaid? Are these funds being spent effectively and efficiently? What are the negative anticipated effects? Asking “and then what” is always a good question, “look before you leap.”

The health of our nation is inextricably linked to the financial health of our government. We rely on efficient, effective public spending for everything from roads and schools to healthcare and national security. A government that mismanages its finances can’t meet the needs of its citizens, and without informed citizens holding it accountable, wasteful spending and inefficiency can become the norm.

Time to Get Engaged

If you think GFL is overwhelming or too difficult, consider the alternatives. Just as you wouldn’t leave your personal financial future in the hands of others without trust and oversight, you wouldn’t hand over the responsibility for our collective financial future without staying informed. Every dollar the government spends is your money— you should know where it’s going.

By taking the time to increase your Government Financial Literacy, you gain the tools to understand and challenge public spending, demand transparency, and ensure your tax dollars are working effectively to strengthen our democracy. It’s time for GFL to become a priority in schools, in public discourse, and in our everyday lives. It’s time for all of us to step up and take responsibility for our country’s financial health which is ultimately our countries health, and our own financial health.

“Democracy cannot succeed unless those who express their choice are prepared to choose wisely. The real safeguard of democracy, therefore, is education.”

Franklin D. Roosevelt

At the Tax Project Institute, we do not engage in advocacy of specific parties, or policies. However, we provide Civic Education, and Facts to help you along your Government Financial Literacy journey.

Tax Project Institute is a fiscally sponsored project of MarinLink, a California non-profit corporation exempt from federal tax under section 501(c)(3) of the Internal Revenue Service #20-0879422.